Workflow#

chainladder facilitates practical reserving workflows.

import chainladder as cl

import numpy as np

import matplotlib.pyplot as plt

plt.style.use('ggplot')

%config InlineBackend.figure_format = 'retina'

Pipeline#

The :class:Pipeline class implements utilities to build a composite

estimator, as a chain of transforms and estimators. Said differently, a

Pipeline is a way to wrap multiple estimators into a single compact object.

The Pipeline is borrowed from scikit-learn. As an example of compactness,

we can simulate a set of triangles using bootstrap sampling, apply volume-weigted

development, exponential tail curve fitting, and get the 95%-ile IBNR estimate.

pipe = cl.Pipeline(

steps=[

('sample', cl.BootstrapODPSample(random_state=42)),

('dev', cl.Development(average='volume')),

('tail', cl.TailCurve('exponential')),

('model', cl.Chainladder())])

pipe.fit(cl.load_sample('genins'))

Pipeline(steps=[('sample', BootstrapODPSample(random_state=42)),

('dev', Development()), ('tail', TailCurve()),

('model', Chainladder())])In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Pipeline(steps=[('sample', BootstrapODPSample(random_state=42)),

('dev', Development()), ('tail', TailCurve()),

('model', Chainladder())])BootstrapODPSample(random_state=42)

Development()

TailCurve()

Chainladder()

Each estimator contained within a pipelines steps can be accessed by name

using the named_steps attribute of the Pipeline.

pipe.named_steps.model.ibnr_.sum('origin').quantile(q=.95)

26063265.93984502

As mentioned in the Development section, a Pipeline coupled with groupby can really streamline you reserving analysis. Here we can develop IBNR for each company using LOB level development patterns. By delegating the groupby operation to the Development estimator in the Pipeline, we can fully specify the entire analysis as part of our hyperparameters. This achieves a clear separation of assumption setting from data manipulation.

clrd = cl.load_sample('clrd')['CumPaidLoss']

pipe = cl.Pipeline(

steps=[

('dev', cl.Development(groupby='LOB')),

('tail', cl.TailCurve('exponential')),

('model', cl.Chainladder())]).fit(clrd)

pipe.named_steps.model.ibnr_

| Triangle Summary | |

|---|---|

| Valuation: | 2261-12 |

| Grain: | OYDY |

| Shape: | (775, 1, 10, 1) |

| Index: | [GRNAME, LOB] |

| Columns: | [CumPaidLoss] |

VotingChainladder#

The :class:VotingChainladder ensemble method allows the actuary to vote between

different underlying ibnr_ by way of a matrix of weights.

For example, the actuary may choose

the :class:

Chainladdermethod for the first 4 origin periods,the :class:

BornhuetterFergusonmethod for the next 3 origin periods,and the :class:

CapeCodmethod for the final 3.

raa = cl.load_sample('RAA')

cl_ult = cl.Chainladder().fit(raa).ultimate_ # Chainladder Ultimate

apriori = cl_ult*0+(cl_ult.sum()/10) # Mean Chainladder Ultimate

bcl = cl.Chainladder()

bf = cl.BornhuetterFerguson()

cc = cl.CapeCod()

estimators = [('bcl', bcl), ('bf', bf), ('cc', cc)]

weights = np.array([[1, 0, 0]] * 4 + [[0, 1, 0]] * 3 + [[0, 0, 1]] * 3)

vot = cl.VotingChainladder(estimators=estimators, weights=weights)

vot.fit(raa, sample_weight=apriori)

vot.ultimate_

| 2261 | |

|---|---|

| 1981 | 18,834 |

| 1982 | 16,858 |

| 1983 | 24,083 |

| 1984 | 28,703 |

| 1985 | 28,204 |

| 1986 | 19,840 |

| 1987 | 18,840 |

| 1988 | 23,107 |

| 1989 | 20,005 |

| 1990 | 21,606 |

Alternatively, the actuary may choose to combine all methods using weights. Omitting

the weights parameter results in the average of all predictions assuming a weight of 1.

Alternatively, a default weight can be enforced through the default_weight parameter.

raa = cl.load_sample('RAA')

cl_ult = cl.Chainladder().fit(raa).ultimate_ # Chainladder Ultimate

apriori = cl_ult * 0 + (float(cl_ult.sum()) / 10) # Mean Chainladder Ultimate

bcl = cl.Chainladder()

bf = cl.BornhuetterFerguson()

cc = cl.CapeCod()

estimators = [('bcl', bcl), ('bf', bf), ('cc', cc)]

vot = cl.VotingChainladder(estimators=estimators)

vot.fit(raa, sample_weight=apriori)

vot.ultimate_

| 2261 | |

|---|---|

| 1981 | 18,834 |

| 1982 | 16,887 |

| 1983 | 24,042 |

| 1984 | 28,436 |

| 1985 | 28,467 |

| 1986 | 19,771 |

| 1987 | 18,548 |

| 1988 | 23,305 |

| 1989 | 18,530 |

| 1990 | 20,331 |

The weights can take the form of an array (as above), a dict, or a callable:

callable_weight = lambda origin : np.where(origin.year < 1985, (1, 0, 0), np.where(origin.year > 1987, (0, 0, 1), (0, 1, 0)))

dict_weight = {

'1992': (0, 1, 0),

'1993': (0, 1, 0),

'1994': (0, 1, 0),

'1995': (0, 0, 1),

'1996': (0, 0, 1),

'1997': (0, 0, 1),

} # Unmapped origins will get `default_weight`

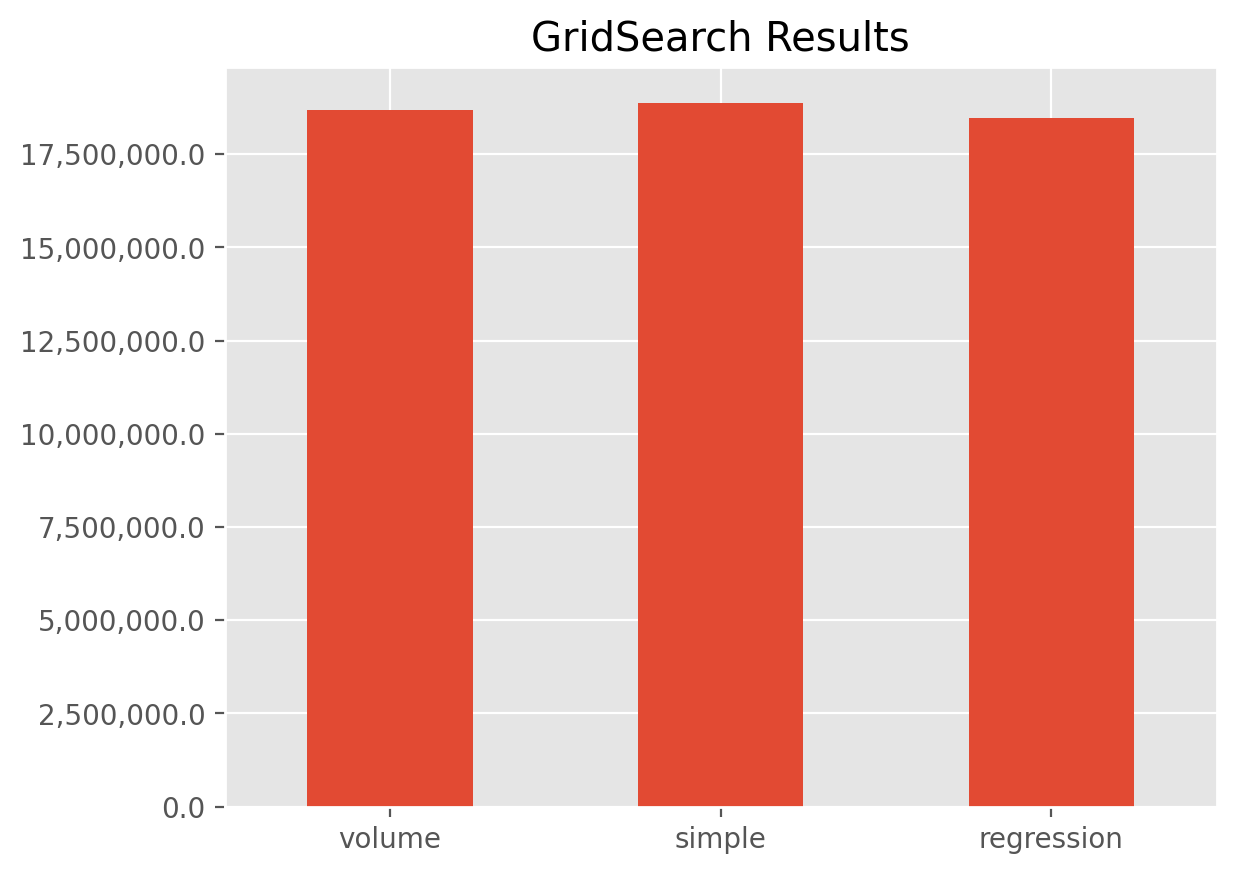

GridSearch#

The grid search provided by :class:GridSearch exhaustively generates

candidates from a grid of parameter values specified with the param_grid

parameter. Like Pipeline, GridSearch borrows from its scikit-learn counterpart

GridSearchCV.

Because reserving techniques are different from supervised machine learning,

GridSearch does not try to pick optimal hyperparameters for you. It is more of

a scenario-testing estimator.

Tip

The tryangle package takes the machine learning aspect a bit farther than chainladder and

has built in scoring functions that make hyperparameter tuning in a reserving context possible.

GridSearch can be applied to all other estimators, including the Pipeline

estimator. To use it, one must specify a param_grid as well as a scoring

function which defines the estimator property(s) you wish to capture.

pipe = cl.Pipeline(

steps=[('dev', cl.Development()),

('model', cl.Chainladder())])

grid = cl.GridSearch(

estimator=pipe,

param_grid={'dev__average' :['volume', 'simple', 'regression']},

scoring=lambda x : x.named_steps.model.ibnr_.sum('origin'))

grid.fit(cl.load_sample('genins'))

ax = grid.results_.set_index('dev__average').rename(columns={'score': 'IBNR'}).plot(

kind='bar', legend=False, xlabel='', rot=0, title='GridSearch Results')

ax.yaxis.set_major_formatter(

plt.FuncFormatter(lambda value, tick_number: "{:,}".format(float(value))));

A couple points on the example.

The syntax for GridSearch is a near replica of scikit-learn’s

GridsearchCVThe

param_gridis a dictionary of hyperparamter names and possible options you may want to use.Multiple different hyperparameters can be specified in a

param_grid. Doing so will create a cartesian product of all possible assumptions.When using a

Pipelinein aGridSearchit is entirely possible that theparam_gridhyperparameter names used in different steps of a thePipelinecan clash. The notation to disambiguate the hyperparameters is to specify both the step and the hyperparameter name in this fashion:step__hyperparameter

Note

All of this can be done with loops, but GridSearch provides a nice shorthand for accomplishing the same as well as parallelism when your CPU has multiple cores.

Your scoring function can be any property derived off of the fitted etimator.

If capturing multiple properties is desired, multiple scoring functions can be created and

stored in a dictionary.

Here we capture multiple properties of the TailBondy estimator using the

GridSearch routine to test the sensitivity of the model to changing hyperparameters.

# Fit basic development to a triangle

tri = cl.load_sample('tail_sample')['paid']

dev = cl.Development(average='simple').fit_transform(tri)

# Return both the tail factor and the Bondy exponent in the scoring function

scoring = {

'Tail Factor (tail_)': lambda x: x.tail_.values[0,0],

'Bondy Exponent (b_)': lambda x : x.b_.values[0,0]}

# Vary the 'earliest_age' assumption in GridSearch

param_grid=dict(earliest_age=list(range(12, 120, 12)))

grid = cl.GridSearch(

estimator=cl.TailBondy(),

param_grid=param_grid,

scoring=scoring)

grid.fit(dev).results_

| earliest_age | Tail Factor (tail_) | Bondy Exponent (b_) | |

|---|---|---|---|

| 0 | 12 | 1.027763 | 0.624614 |

| 1 | 24 | 1.027983 | 0.625014 |

| 2 | 36 | 1.029856 | 0.629534 |

| 3 | 48 | 1.037931 | 0.651859 |

| 4 | 60 | 1.048890 | 0.683528 |

| 5 | 72 | 1.046617 | 0.674587 |

| 6 | 84 | 1.059931 | 0.714418 |

| 7 | 96 | 1.072279 | 0.746943 |

| 8 | 108 | 1.023925 | 0.500000 |

Using GridSearch for scenario testing is entirely optional. You can write

your own looping mechanisms to achieve the same result. For example:

It is also possible to treat estimators themselves as hyperparameters. A GridSearch can search over Chainladder and CapeCod or any other estimator. To achieve this, you can take your param_grid dictionary and make it a list of dictionaries.

clrd = cl.load_sample('clrd')[['CumPaidLoss', 'EarnedPremDIR']].groupby('LOB').sum().loc['medmal']

grid = cl.GridSearch(

estimator = cl.Pipeline(steps=[

('dev', None),

('model', None)]),

param_grid = [

{'dev': [cl.Development()],

'dev__n_periods': [-1, 3, 7],

'model': [cl.Chainladder()]},

{'dev': [cl.Development()],

'dev__n_periods': [-1, 3, 7],

'model': [cl.CapeCod()],

'model__decay': [0, .5, 1]}],

scoring=lambda x : x.named_steps.model.ibnr_.sum('origin')

)

grid.fit(

X=clrd['CumPaidLoss'],

sample_weight=clrd['EarnedPremDIR'].latest_diagonal)

grid.results_

| dev | dev__n_periods | model | score | model__decay | |

|---|---|---|---|---|---|

| 0 | Development(n_periods=7) | -1 | Chainladder() | 1.330331e+06 | NaN |

| 1 | Development(n_periods=7) | 3 | Chainladder() | 1.254405e+06 | NaN |

| 2 | Development(n_periods=7) | 7 | Chainladder() | 1.321097e+06 | NaN |

| 3 | Development(n_periods=7) | -1 | CapeCod() | 1.330331e+06 | 0.0 |

| 4 | Development(n_periods=7) | -1 | CapeCod() | 1.278456e+06 | 0.5 |

| 5 | Development(n_periods=7) | -1 | CapeCod() | 1.066857e+06 | 1.0 |

| 6 | Development(n_periods=7) | 3 | CapeCod() | 1.254405e+06 | 0.0 |

| 7 | Development(n_periods=7) | 3 | CapeCod() | 1.225866e+06 | 0.5 |

| 8 | Development(n_periods=7) | 3 | CapeCod() | 1.040709e+06 | 1.0 |

| 9 | Development(n_periods=7) | 7 | CapeCod() | 1.321097e+06 | 0.0 |

| 10 | Development(n_periods=7) | 7 | CapeCod() | 1.276399e+06 | 0.5 |

| 11 | Development(n_periods=7) | 7 | CapeCod() | 1.066171e+06 | 1.0 |

The workflow estimators are incredibly flexible for composing any compound reserving workflow into a single estimator. These succintly capture all “assumptions” and model definitions in one place.