Applying Deterministic Methods#

Getting Started#

This tutorial focuses on using deterministic methods to square a triangle.

Be sure to make sure your packages are updated. For more info on how to update your pakages, visit Keeping Packages Updated.

# Black linter, optional

%load_ext lab_black

import pandas as pd

import numpy as np

import chainladder as cl

import matplotlib.pyplot as plt

print("pandas: " + pd.__version__)

print("numpy: " + np.__version__)

print("chainladder: " + cl.__version__)

pandas: 2.1.4

numpy: 1.24.3

chainladder: 0.8.18

Disclaimer#

Note that a lot of the examples shown might not be applicable in a real world scenario, and is only meant to demonstrate some of the functionalities included in the package. The user should always follow all applicable laws, the Code of Professional Conduct, applicable Actuarial Standards of Practice, and exercise their best actuarial judgement.

Chainladder Method#

The basic chainladder method is entirely specified by its development pattern selections. For this reason, the Chainladder estimator takes no additional assumptions, i.e. no additional arguments. Let’s start by loading an example dataset and creating an Triangle with Development patterns and a TailCurve. Recall, we can bundle these two estimators into a single Pipeline if we wish.

genins = cl.load_sample("genins")

genins_dev = cl.Pipeline(

[("dev", cl.Development()), ("tail", cl.TailCurve())]

).fit_transform(genins)

We can now use the basic Chainladder estimator to estimate ultimate_ values of our Triangle.

genins_model = cl.Chainladder().fit(genins_dev)

genins_model.ultimate_

| 2261 | |

|---|---|

| 2001 | 4,016,553 |

| 2002 | 5,594,009 |

| 2003 | 5,537,497 |

| 2004 | 5,454,190 |

| 2005 | 5,001,513 |

| 2006 | 5,261,947 |

| 2007 | 5,827,759 |

| 2008 | 6,984,945 |

| 2009 | 5,808,708 |

| 2010 | 5,116,430 |

We can also view the ibnr_. Techincally the term IBNR is reserved for Incurred but not Reported, but the chainladder models use it to describe the difference between the ultimate and the latest evaluation period.

genins_model.ibnr_

| 2261 | |

|---|---|

| 2001 | 115,090 |

| 2002 | 254,924 |

| 2003 | 628,182 |

| 2004 | 865,922 |

| 2005 | 1,128,202 |

| 2006 | 1,570,235 |

| 2007 | 2,344,629 |

| 2008 | 4,120,447 |

| 2009 | 4,445,414 |

| 2010 | 4,772,416 |

It is often useful to see the completed Triangle and this can be accomplished by inspecting the full_triangle_. As with most other estimator properties, the full_triangle_ is itself a Triangle and can be manipulated as such.

genins

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 357,848 | 1,124,788 | 1,735,330 | 2,218,270 | 2,745,596 | 3,319,994 | 3,466,336 | 3,606,286 | 3,833,515 | 3,901,463 |

| 2002 | 352,118 | 1,236,139 | 2,170,033 | 3,353,322 | 3,799,067 | 4,120,063 | 4,647,867 | 4,914,039 | 5,339,085 | |

| 2003 | 290,507 | 1,292,306 | 2,218,525 | 3,235,179 | 3,985,995 | 4,132,918 | 4,628,910 | 4,909,315 | ||

| 2004 | 310,608 | 1,418,858 | 2,195,047 | 3,757,447 | 4,029,929 | 4,381,982 | 4,588,268 | |||

| 2005 | 443,160 | 1,136,350 | 2,128,333 | 2,897,821 | 3,402,672 | 3,873,311 | ||||

| 2006 | 396,132 | 1,333,217 | 2,180,715 | 2,985,752 | 3,691,712 | |||||

| 2007 | 440,832 | 1,288,463 | 2,419,861 | 3,483,130 | ||||||

| 2008 | 359,480 | 1,421,128 | 2,864,498 | |||||||

| 2009 | 376,686 | 1,363,294 | ||||||||

| 2010 | 344,014 |

genins_model.full_triangle_

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | 132 | 9999 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 357,848 | 1,124,788 | 1,735,330 | 2,218,270 | 2,745,596 | 3,319,994 | 3,466,336 | 3,606,286 | 3,833,515 | 3,901,463 | 3,948,071 | 4,016,553 |

| 2002 | 352,118 | 1,236,139 | 2,170,033 | 3,353,322 | 3,799,067 | 4,120,063 | 4,647,867 | 4,914,039 | 5,339,085 | 5,433,719 | 5,498,632 | 5,594,009 |

| 2003 | 290,507 | 1,292,306 | 2,218,525 | 3,235,179 | 3,985,995 | 4,132,918 | 4,628,910 | 4,909,315 | 5,285,148 | 5,378,826 | 5,443,084 | 5,537,497 |

| 2004 | 310,608 | 1,418,858 | 2,195,047 | 3,757,447 | 4,029,929 | 4,381,982 | 4,588,268 | 4,835,458 | 5,205,637 | 5,297,906 | 5,361,197 | 5,454,190 |

| 2005 | 443,160 | 1,136,350 | 2,128,333 | 2,897,821 | 3,402,672 | 3,873,311 | 4,207,459 | 4,434,133 | 4,773,589 | 4,858,200 | 4,916,237 | 5,001,513 |

| 2006 | 396,132 | 1,333,217 | 2,180,715 | 2,985,752 | 3,691,712 | 4,074,999 | 4,426,546 | 4,665,023 | 5,022,155 | 5,111,171 | 5,172,231 | 5,261,947 |

| 2007 | 440,832 | 1,288,463 | 2,419,861 | 3,483,130 | 4,088,678 | 4,513,179 | 4,902,528 | 5,166,649 | 5,562,182 | 5,660,771 | 5,728,396 | 5,827,759 |

| 2008 | 359,480 | 1,421,128 | 2,864,498 | 4,174,756 | 4,900,545 | 5,409,337 | 5,875,997 | 6,192,562 | 6,666,635 | 6,784,799 | 6,865,853 | 6,984,945 |

| 2009 | 376,686 | 1,363,294 | 2,382,128 | 3,471,744 | 4,075,313 | 4,498,426 | 4,886,502 | 5,149,760 | 5,544,000 | 5,642,266 | 5,709,671 | 5,808,708 |

| 2010 | 344,014 | 1,200,818 | 2,098,228 | 3,057,984 | 3,589,620 | 3,962,307 | 4,304,132 | 4,536,015 | 4,883,270 | 4,969,825 | 5,029,196 | 5,116,430 |

genins_model.full_triangle_.dev_to_val()

| 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | ... | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2261 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 357,848 | 1,124,788 | 1,735,330 | 2,218,270 | 2,745,596 | 3,319,994 | 3,466,336 | 3,606,286 | 3,833,515 | 3,901,463 | ... | 3,948,071 | 3,948,071 | 3,948,071 | 3,948,071 | 3,948,071 | 3,948,071 | 3,948,071 | 3,948,071 | 3,948,071 | 4,016,553 |

| 2002 | 352,118 | 1,236,139 | 2,170,033 | 3,353,322 | 3,799,067 | 4,120,063 | 4,647,867 | 4,914,039 | 5,339,085 | ... | 5,498,632 | 5,498,632 | 5,498,632 | 5,498,632 | 5,498,632 | 5,498,632 | 5,498,632 | 5,498,632 | 5,498,632 | 5,594,009 | |

| 2003 | 290,507 | 1,292,306 | 2,218,525 | 3,235,179 | 3,985,995 | 4,132,918 | 4,628,910 | 4,909,315 | ... | 5,378,826 | 5,443,084 | 5,443,084 | 5,443,084 | 5,443,084 | 5,443,084 | 5,443,084 | 5,443,084 | 5,443,084 | 5,537,497 | ||

| 2004 | 310,608 | 1,418,858 | 2,195,047 | 3,757,447 | 4,029,929 | 4,381,982 | 4,588,268 | ... | 5,205,637 | 5,297,906 | 5,361,197 | 5,361,197 | 5,361,197 | 5,361,197 | 5,361,197 | 5,361,197 | 5,361,197 | 5,454,190 | |||

| 2005 | 443,160 | 1,136,350 | 2,128,333 | 2,897,821 | 3,402,672 | 3,873,311 | ... | 4,434,133 | 4,773,589 | 4,858,200 | 4,916,237 | 4,916,237 | 4,916,237 | 4,916,237 | 4,916,237 | 4,916,237 | 5,001,513 | ||||

| 2006 | 396,132 | 1,333,217 | 2,180,715 | 2,985,752 | 3,691,712 | ... | 4,426,546 | 4,665,023 | 5,022,155 | 5,111,171 | 5,172,231 | 5,172,231 | 5,172,231 | 5,172,231 | 5,172,231 | 5,261,947 | |||||

| 2007 | 440,832 | 1,288,463 | 2,419,861 | 3,483,130 | ... | 4,513,179 | 4,902,528 | 5,166,649 | 5,562,182 | 5,660,771 | 5,728,396 | 5,728,396 | 5,728,396 | 5,728,396 | 5,827,759 | ||||||

| 2008 | 359,480 | 1,421,128 | 2,864,498 | ... | 4,900,545 | 5,409,337 | 5,875,997 | 6,192,562 | 6,666,635 | 6,784,799 | 6,865,853 | 6,865,853 | 6,865,853 | 6,984,945 | |||||||

| 2009 | 376,686 | 1,363,294 | ... | 3,471,744 | 4,075,313 | 4,498,426 | 4,886,502 | 5,149,760 | 5,544,000 | 5,642,266 | 5,709,671 | 5,709,671 | 5,808,708 | ||||||||

| 2010 | 344,014 | ... | 2,098,228 | 3,057,984 | 3,589,620 | 3,962,307 | 4,304,132 | 4,536,015 | 4,883,270 | 4,969,825 | 5,029,196 | 5,116,430 |

Notice the calendar year of our ultimates. While ultimates will generally be realized before this date, the chainladder package picks the highest allowable date available for its ultimate_ valuation.

genins_model.full_triangle_.valuation_date

Timestamp('2261-12-31 23:59:59.999999999')

We can further manipulate the “triangle”, such as applying cum_to_incr().

genins_model.full_triangle_.dev_to_val().cum_to_incr()

| 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | ... | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2261 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 357,848 | 766,940 | 610,542 | 482,940 | 527,326 | 574,398 | 146,342 | 139,950 | 227,229 | 67,948 | ... | 68,482 | |||||||||

| 2002 | 352,118 | 884,021 | 933,894 | 1,183,289 | 445,745 | 320,996 | 527,804 | 266,172 | 425,046 | ... | 64,913 | 95,377 | |||||||||

| 2003 | 290,507 | 1,001,799 | 926,219 | 1,016,654 | 750,816 | 146,923 | 495,992 | 280,405 | ... | 93,678 | 64,257 | 94,413 | |||||||||

| 2004 | 310,608 | 1,108,250 | 776,189 | 1,562,400 | 272,482 | 352,053 | 206,286 | ... | 370,179 | 92,268 | 63,291 | 92,993 | |||||||||

| 2005 | 443,160 | 693,190 | 991,983 | 769,488 | 504,851 | 470,639 | ... | 226,674 | 339,456 | 84,611 | 58,038 | 85,275 | |||||||||

| 2006 | 396,132 | 937,085 | 847,498 | 805,037 | 705,960 | ... | 351,548 | 238,477 | 357,132 | 89,016 | 61,060 | 89,715 | |||||||||

| 2007 | 440,832 | 847,631 | 1,131,398 | 1,063,269 | ... | 424,501 | 389,349 | 264,121 | 395,534 | 98,588 | 67,626 | 99,362 | |||||||||

| 2008 | 359,480 | 1,061,648 | 1,443,370 | ... | 725,788 | 508,792 | 466,660 | 316,566 | 474,073 | 118,164 | 81,054 | 119,092 | |||||||||

| 2009 | 376,686 | 986,608 | ... | 1,089,616 | 603,569 | 423,113 | 388,076 | 263,257 | 394,241 | 98,266 | 67,405 | 99,038 | |||||||||

| 2010 | 344,014 | ... | 897,410 | 959,756 | 531,636 | 372,687 | 341,826 | 231,882 | 347,255 | 86,555 | 59,371 | 87,234 |

Another useful property is full_expectation_. Similar to the full_triangle, it “squares” the Triangle, but replaces the known data with expected values implied by the model and development pattern.

genins_model.full_expectation_

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | 132 | 9999 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 270,061 | 942,678 | 1,647,172 | 2,400,610 | 2,817,960 | 3,110,531 | 3,378,874 | 3,560,909 | 3,833,515 | 3,901,463 | 3,948,071 | 4,016,553 |

| 2002 | 376,125 | 1,312,904 | 2,294,081 | 3,343,423 | 3,924,682 | 4,332,157 | 4,705,889 | 4,959,416 | 5,339,085 | 5,433,719 | 5,498,632 | 5,594,009 |

| 2003 | 372,325 | 1,299,641 | 2,270,905 | 3,309,647 | 3,885,035 | 4,288,393 | 4,658,349 | 4,909,315 | 5,285,148 | 5,378,826 | 5,443,084 | 5,537,497 |

| 2004 | 366,724 | 1,280,089 | 2,236,741 | 3,259,856 | 3,826,587 | 4,223,877 | 4,588,268 | 4,835,458 | 5,205,637 | 5,297,906 | 5,361,197 | 5,454,190 |

| 2005 | 336,287 | 1,173,846 | 2,051,100 | 2,989,300 | 3,508,995 | 3,873,311 | 4,207,459 | 4,434,133 | 4,773,589 | 4,858,200 | 4,916,237 | 5,001,513 |

| 2006 | 353,798 | 1,234,970 | 2,157,903 | 3,144,956 | 3,691,712 | 4,074,999 | 4,426,546 | 4,665,023 | 5,022,155 | 5,111,171 | 5,172,231 | 5,261,947 |

| 2007 | 391,842 | 1,367,765 | 2,389,941 | 3,483,130 | 4,088,678 | 4,513,179 | 4,902,528 | 5,166,649 | 5,562,182 | 5,660,771 | 5,728,396 | 5,827,759 |

| 2008 | 469,648 | 1,639,355 | 2,864,498 | 4,174,756 | 4,900,545 | 5,409,337 | 5,875,997 | 6,192,562 | 6,666,635 | 6,784,799 | 6,865,853 | 6,984,945 |

| 2009 | 390,561 | 1,363,294 | 2,382,128 | 3,471,744 | 4,075,313 | 4,498,426 | 4,886,502 | 5,149,760 | 5,544,000 | 5,642,266 | 5,709,671 | 5,808,708 |

| 2010 | 344,014 | 1,200,818 | 2,098,228 | 3,057,984 | 3,589,620 | 3,962,307 | 4,304,132 | 4,536,015 | 4,883,270 | 4,969,825 | 5,029,196 | 5,116,430 |

With some clever arithmetic, we can use these objects to give us other useful information. For example, we can retrospectively review the actual Triangle against its modeled expectation.

genins_model.full_triangle_ - genins_model.full_expectation_

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | 132 | 9999 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 87,787 | 182,110 | 88,158 | -182,340 | -72,364 | 209,463 | 87,462 | 45,377 | 0 | |||

| 2002 | -24,007 | -76,765 | -124,048 | 9,899 | -125,615 | -212,094 | -58,022 | -45,377 | ||||

| 2003 | -81,818 | -7,335 | -52,380 | -74,468 | 100,960 | -155,475 | -29,439 | -0 | ||||

| 2004 | -56,116 | 138,769 | -41,694 | 497,591 | 203,342 | 158,105 | 0 | |||||

| 2005 | 106,873 | -37,496 | 77,233 | -91,479 | -106,323 | 0 | 0 | 0 | ||||

| 2006 | 42,334 | 98,247 | 22,812 | -159,204 | 0 | 0 | ||||||

| 2007 | 48,990 | -79,302 | 29,920 | 0 | 0 | 0 | 0 | |||||

| 2008 | -110,168 | -218,227 | 0 | 0 | 0 | |||||||

| 2009 | -13,875 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||

| 2010 | 0 | 0 | 0 | 0 | 0 |

We can also filter out the lower right part of the triangle with [genins_model.full_triangle_.valuation <= genins.valuation_date].

(

genins_model.full_triangle_[

genins_model.full_triangle_.valuation <= genins.valuation_date

]

- genins_model.full_expectation_[

genins_model.full_triangle_.valuation <= genins.valuation_date

]

)

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 87,787 | 182,110 | 88,158 | -182,340 | -72,364 | 209,463 | 87,462 | 45,377 | 0 | |

| 2002 | -24,007 | -76,765 | -124,048 | 9,899 | -125,615 | -212,094 | -58,022 | -45,377 | ||

| 2003 | -81,818 | -7,335 | -52,380 | -74,468 | 100,960 | -155,475 | -29,439 | |||

| 2004 | -56,116 | 138,769 | -41,694 | 497,591 | 203,342 | 158,105 | ||||

| 2005 | 106,873 | -37,496 | 77,233 | -91,479 | -106,323 | |||||

| 2006 | 42,334 | 98,247 | 22,812 | -159,204 | ||||||

| 2007 | 48,990 | -79,302 | 29,920 | |||||||

| 2008 | -110,168 | -218,227 | ||||||||

| 2009 | -13,875 | |||||||||

| 2010 |

Getting comfortable with manipulating Triangles will greatly improve our ability to extract value out of the chainladder package. Here is another way of getting the same answer.

genins_AvE = genins - genins_model.full_expectation_

genins_AvE[genins_AvE.valuation <= genins.valuation_date]

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 87,787 | 182,110 | 88,158 | -182,340 | -72,364 | 209,463 | 87,462 | 45,377 | 0 | |

| 2002 | -24,007 | -76,765 | -124,048 | 9,899 | -125,615 | -212,094 | -58,022 | -45,377 | ||

| 2003 | -81,818 | -7,335 | -52,380 | -74,468 | 100,960 | -155,475 | -29,439 | |||

| 2004 | -56,116 | 138,769 | -41,694 | 497,591 | 203,342 | 158,105 | ||||

| 2005 | 106,873 | -37,496 | 77,233 | -91,479 | -106,323 | |||||

| 2006 | 42,334 | 98,247 | 22,812 | -159,204 | ||||||

| 2007 | 48,990 | -79,302 | 29,920 | |||||||

| 2008 | -110,168 | -218,227 | ||||||||

| 2009 | -13,875 | |||||||||

| 2010 |

We can also filter out the lower right part of the triangle with [genins_model.full_triangle_.valuation <= genins.valuation_date] before applying the heatmap().

genins_AvE[genins_AvE.valuation <= genins.valuation_date].heatmap()

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 87,787 | 182,110 | 88,158 | -182,340 | -72,364 | 209,463 | 87,462 | 45,377 | 0 | |

| 2002 | -24,007 | -76,765 | -124,048 | 9,899 | -125,615 | -212,094 | -58,022 | -45,377 | ||

| 2003 | -81,818 | -7,335 | -52,380 | -74,468 | 100,960 | -155,475 | -29,439 | |||

| 2004 | -56,116 | 138,769 | -41,694 | 497,591 | 203,342 | 158,105 | ||||

| 2005 | 106,873 | -37,496 | 77,233 | -91,479 | -106,323 | |||||

| 2006 | 42,334 | 98,247 | 22,812 | -159,204 | ||||||

| 2007 | 48,990 | -79,302 | 29,920 | |||||||

| 2008 | -110,168 | -218,227 | ||||||||

| 2009 | -13,875 | |||||||||

| 2010 |

Can you figure out how to get the expected IBNR runoff in the upcoming year?

cal_yr_ibnr = genins_model.full_triangle_.dev_to_val().cum_to_incr()

cal_yr_ibnr[cal_yr_ibnr.valuation.year == 2011]

| 2011 | |

|---|---|

| 2001 | 46,608 |

| 2002 | 94,634 |

| 2003 | 375,833 |

| 2004 | 247,190 |

| 2005 | 334,148 |

| 2006 | 383,287 |

| 2007 | 605,548 |

| 2008 | 1,310,258 |

| 2009 | 1,018,834 |

| 2010 | 856,804 |

Expected Loss Method#

Next, let’s talk about the expected loss method, where we know the ultimate loss already (but then why are you trying to estimate your ultimate losses?). The ExpectedLoss model estimator has many of the same attributes as the Chainladder estimator. It comes with one input assumption, the a priori (apriori). This is a scalar multiplier that will be applied to an exposure vector, which will produce an a priori ultimate estimate vector that we can use for the model.

Earlier, we used the Chainladder method on the genins data. Let’s use the average of the Chainladder ultimate to help us derive an a priori in the expected loss method.

Below, we use genins_model.ultimate_ * 0 and add the mean to it to preserve the index values of years 2001 - 2020.

expected_loss_apriori = genins_model.ultimate_ * 0 + genins_model.ultimate_.mean()

expected_loss_apriori

| 2261 | |

|---|---|

| 2001 | 5,460,355 |

| 2002 | 5,460,355 |

| 2003 | 5,460,355 |

| 2004 | 5,460,355 |

| 2005 | 5,460,355 |

| 2006 | 5,460,355 |

| 2007 | 5,460,355 |

| 2008 | 5,460,355 |

| 2009 | 5,460,355 |

| 2010 | 5,460,355 |

Let’s assume that we know our expected loss will be 95% of the a priori, which is common if the a priori is a function of something else, like earned premium. We set apriori with 0.95 inside the function, then call fit on the data, genins, and assigh the sample_weight with our vector of a prioris, expected_loss_apriori.

EL_model = cl.ExpectedLoss(apriori=0.95).fit(

genins, sample_weight=expected_loss_apriori

)

EL_model.ultimate_

| 2261 | |

|---|---|

| 2001 | 5,187,337 |

| 2002 | 5,187,337 |

| 2003 | 5,187,337 |

| 2004 | 5,187,337 |

| 2005 | 5,187,337 |

| 2006 | 5,187,337 |

| 2007 | 5,187,337 |

| 2008 | 5,187,337 |

| 2009 | 5,187,337 |

| 2010 | 5,187,337 |

Bornhuetter-Ferguson Method#

The BornhuetterFerguson estimator is another deterministic method having many of the same attributes as the Chainladder estimator. It comes with one input assumption, the a priori (apriori). This is a scalar multiplier that will be applied to an exposure vector, which will produce an a priori ultimate estimate vector that we can use for the model.

Since the CAS Loss Reserve Database has premium, we will use it as an example. Let’s grab the paid loss and net earned premium for the commercial auto line of business.

Remember that apriori is a scaler, which we need to apply it to a vector of exposures. Let’s assume that the a priori is 0.75, for 75% loss ratio.

Let’s set an apriori Loss Ratio estimate of 75%

The BornhuetterFerguson method along with all other expected loss methods like CapeCod and Benktander (discussed later), need to take in an exposure vector. The exposure vector has to be a Triangle itself. Remember that the Triangle class supports single exposure vectors.

comauto = cl.load_sample("clrd").groupby("LOB").sum().loc["comauto"]

bf_model = cl.BornhuetterFerguson(apriori=0.75)

bf_model.fit(

comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

BornhuetterFerguson(apriori=0.75)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

BornhuetterFerguson(apriori=0.75)

bf_model.ultimate_

| 2261 | |

|---|---|

| 1988 | 626,097 |

| 1989 | 679,224 |

| 1990 | 728,363 |

| 1991 | 729,927 |

| 1992 | 767,610 |

| 1993 | 833,686 |

| 1994 | 918,582 |

| 1995 | 954,377 |

| 1996 | 985,280 |

| 1997 | 1,031,637 |

Having an apriori that takes on only a constant for all origins can be limiting. This shouldn’t stop the practitioner from exploiting the fact that the apriori can be embedded directly in the exposure vector itself allowing full cusomization of the apriori.

b1 = cl.BornhuetterFerguson(apriori=0.75).fit(

comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

b2 = cl.BornhuetterFerguson(apriori=1.00).fit(

comauto["CumPaidLoss"],

sample_weight=0.75 * comauto["EarnedPremNet"].latest_diagonal,

)

b1.ultimate_ == b2.ultimate_

True

If we need to create a new colume, such as AdjEarnedPrmNet with varying implied loss ratios. It is recommend that we perform any data modification in pandas instead of Triangle forms.

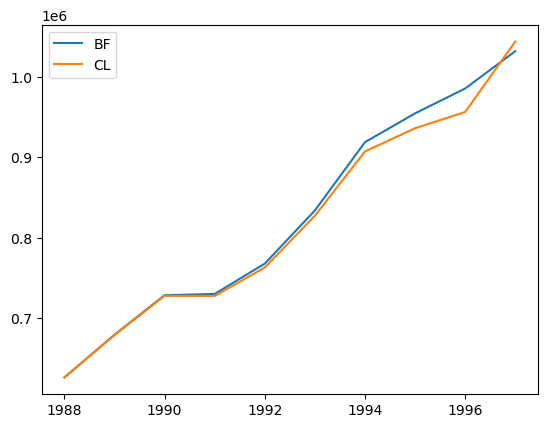

Let’s perform the estimate using Chainladder and compare the results.

bf_model.ultimate_.to_frame(origin_as_datetime=True).index.year

Index([1988, 1989, 1990, 1991, 1992, 1993, 1994, 1995, 1996, 1997], dtype='int32')

plt.plot(

bf_model.ultimate_.to_frame(origin_as_datetime=True).index.year,

bf_model.ultimate_.to_frame(origin_as_datetime=True),

label="BF",

)

cl_model = cl.Chainladder().fit(comauto["CumPaidLoss"])

plt.plot(

cl_model.ultimate_.to_frame(origin_as_datetime=True).index.year,

cl_model.ultimate_.to_frame(origin_as_datetime=True),

label="CL",

)

plt.legend(loc="upper left")

<matplotlib.legend.Legend at 0x7f9fdc2c6e50>

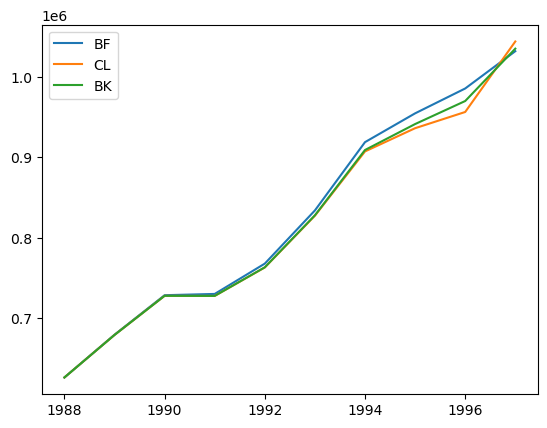

Benktander Method#

The Benktander method is similar to the BornhuetterFerguson method, but allows for the specification of one additional assumption, n_iters, the number of iterations to recalculate the ultimates. The Benktander method generalizes both the BornhuetterFerguson and the Chainladder estimator through this assumption.

When

n_iters = 1, the result is equivalent to theBornhuetterFergusonestimator.When

n_itersis sufficiently large, the result converges to theChainladderestimator.

bk_model = cl.Benktander(apriori=0.75, n_iters=2)

bk_model.fit(

comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

Benktander(apriori=0.75, n_iters=2)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Benktander(apriori=0.75, n_iters=2)

Fitting the Benktander method looks identical to the other methods.

bk_model.fit(

X=comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

Benktander(apriori=0.75, n_iters=2)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Benktander(apriori=0.75, n_iters=2)

plt.plot(

bf_model.ultimate_.to_frame(origin_as_datetime=True).index.year,

bf_model.ultimate_.to_frame(origin_as_datetime=True),

label="BF",

)

plt.plot(

cl_model.ultimate_.to_frame(origin_as_datetime=True).index.year,

cl_model.ultimate_.to_frame(origin_as_datetime=True),

label="CL",

)

plt.plot(

bk_model.ultimate_.to_frame(origin_as_datetime=True).index.year,

bk_model.ultimate_.to_frame(origin_as_datetime=True),

label="BK",

)

plt.legend(loc="upper left")

<matplotlib.legend.Legend at 0x7f9fdc1c2d90>

Cape Cod Method#

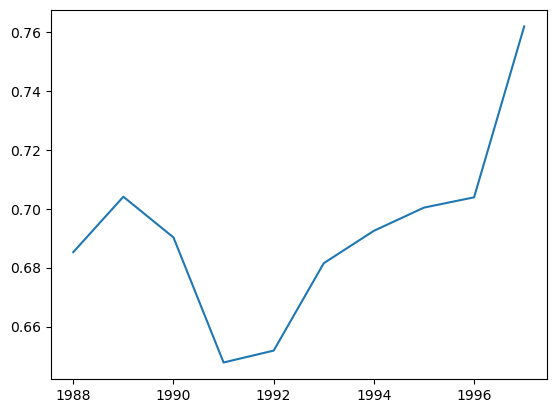

The CapeCod method is similar to the BornhuetterFerguson method, except its apriori is computed from the Triangle itself. Instead of specifying an apriori, decay and trend need to be specified.

decayis the rate that gives weights to earlier origin periods, this parameter is required by the Generalized Cape Cod Method, as discussed in Using Best Practices to Determine a Best Reserve Estimate by Struzzieri and Hussian. As thedecayfactor approaches 1 (the default value), the result approaches the traditional Cape Cod method. As thedecayfactor approaches 0, the result approaches theChainladdermethod.trendis the trend rate along the origin axis to reflect systematic inflationary impacts on the a priori.

When we fit a CapeCod method, we can see the apriori it computes with the given decay and trend assumptions. Since it is an array of estimated parameters, this CapeCod attribute is called the apriori_, with a trailing underscore.

cc_model = cl.CapeCod()

cc_model.fit(

comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

CapeCod()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

CapeCod()

With decay=1, each origin period gets the same apriori_ (this is the traditional Cape Cod). The apriori_ is calculated using the latest diagonal over the used-up exposure, where the used-up exposure is the exposure vector / CDF. Let’s validate the calculation of the a priori.

latest_diagonal = comauto["CumPaidLoss"].latest_diagonal

cdf_as_origin_vector = (

cl.Chainladder().fit(comauto["CumPaidLoss"]).ultimate_

/ comauto["CumPaidLoss"].latest_diagonal

)

latest_diagonal.sum() / (

comauto["EarnedPremNet"].latest_diagonal / cdf_as_origin_vector

).sum()

0.6856862224535671

With decay=0, the apriori_ for each origin period stands on its own.

cc_model = cl.CapeCod(decay=0, trend=0).fit(

X=comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

cc_model.apriori_

| 2261 | |

|---|---|

| 1988 | 0.6853 |

| 1989 | 0.7041 |

| 1990 | 0.6903 |

| 1991 | 0.6478 |

| 1992 | 0.6518 |

| 1993 | 0.6815 |

| 1994 | 0.6925 |

| 1995 | 0.7004 |

| 1996 | 0.7039 |

| 1997 | 0.7619 |

Doing the same on our manually calculated apriori_ yields the same result.

latest_diagonal / (comauto["EarnedPremNet"].latest_diagonal / cdf_as_origin_vector)

| 1997 | |

|---|---|

| 1988 | 0.6853 |

| 1989 | 0.7041 |

| 1990 | 0.6903 |

| 1991 | 0.6478 |

| 1992 | 0.6518 |

| 1993 | 0.6815 |

| 1994 | 0.6925 |

| 1995 | 0.7004 |

| 1996 | 0.7039 |

| 1997 | 0.7619 |

Let’s verify the result of this Cape Cod model’s result with the Chainladder’s.

cc_model.ultimate_ - cl_model.ultimate_

| 2261 | |

|---|---|

| 1988 | |

| 1989 | |

| 1990 | |

| 1991 | |

| 1992 | 0.0000 |

| 1993 | 0.0000 |

| 1994 | |

| 1995 | 0.0000 |

| 1996 | |

| 1997 | 0.0000 |

We can examine the apriori_s to see whether there exhibit any trends over time.

plt.plot(

cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

cc_model.apriori_.to_frame(origin_as_datetime=True),

)

[<matplotlib.lines.Line2D at 0x7f9fdc0153d0>]

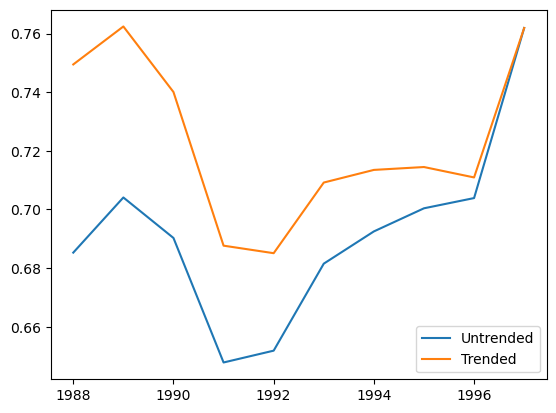

Looks like there is a small positive trend, let’s judgementally select the trend as 1%.

trended_cc_model = cl.CapeCod(decay=0, trend=0.01).fit(

X=comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

plt.plot(

cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

cc_model.apriori_.to_frame(origin_as_datetime=True),

label="Untrended",

)

plt.plot(

trended_cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

trended_cc_model.apriori_.to_frame(origin_as_datetime=True),

label="Trended",

)

plt.legend(loc="lower right")

<matplotlib.legend.Legend at 0x7f9fdc05b3d0>

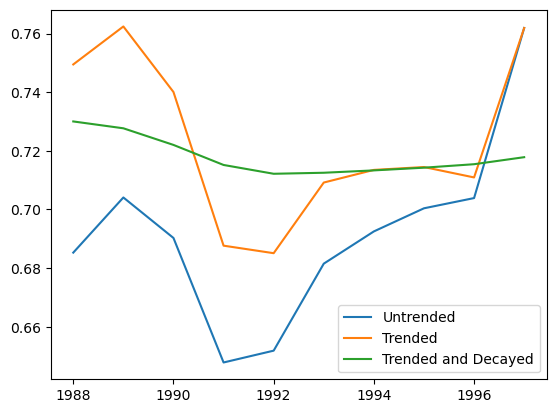

We can of course utilize both the trend and the decay parameters together. Adding trend to the CapeCod method is intended to adjust the apriori_s to a common level. Once at a common level, the apriori_ can be estimated from multiple origin periods using the decay factor.

trended_cc_model = cl.CapeCod(decay=0, trend=0.01).fit(

X=comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

trended_decayed_cc_model = cl.CapeCod(decay=0.75, trend=0.01).fit(

X=comauto["CumPaidLoss"], sample_weight=comauto["EarnedPremNet"].latest_diagonal

)

plt.plot(

cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

cc_model.apriori_.to_frame(origin_as_datetime=True),

label="Untrended",

)

plt.plot(

trended_cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

trended_cc_model.apriori_.to_frame(origin_as_datetime=True),

label="Trended",

)

plt.plot(

trended_decayed_cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

trended_decayed_cc_model.apriori_.to_frame(origin_as_datetime=True),

label="Trended and Decayed",

)

plt.legend(loc="lower right")

<matplotlib.legend.Legend at 0x7f9fdb7aad90>

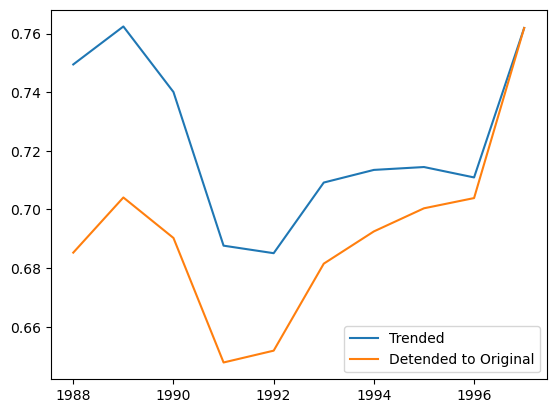

Once estimated, it is necessary to detrend our apriori_s back to their untrended levels and these are contained in detrended_apriori_. It is the detrended_apriori_ that gets used in the calculation of ultimate_ losses.

plt.plot(

trended_cc_model.apriori_.to_frame(origin_as_datetime=True).index.year,

trended_cc_model.apriori_.to_frame(origin_as_datetime=True),

label="Trended",

)

plt.plot(

trended_cc_model.detrended_apriori_.to_frame(origin_as_datetime=True).index.year,

trended_cc_model.detrended_apriori_.to_frame(origin_as_datetime=True),

label="Detended to Original",

)

plt.legend(loc="lower right")

<matplotlib.legend.Legend at 0x7f9fdb663e50>

The detrended_apriori_ is a much smoother estimate of the initial expected ultimate_. With the detrended_apriori_ in hand, the CapeCod method estimator behaves exactly like our the BornhuetterFerguson model.

bf_model = cl.BornhuetterFerguson().fit(

X=comauto["CumPaidLoss"],

sample_weight=trended_cc_model.detrended_apriori_

* comauto["EarnedPremNet"].latest_diagonal,

)

bf_model.ultimate_.sum() == trended_cc_model.ultimate_.sum()

True

Recap#

All the deterministic estimators have ultimate_, ibnr_, full_expecation_ and full_triangle_ attributes that are themselves Triangles. These can be manipulated in a variety of ways to gain additional insights from our model. The expected loss methods take in an exposure vector, which itself is a Triangle through the sample_weight argument of the fit method. The CapeCod method has the additional attributes apriori_ and detrended_apriori_ to accommodate the selection of its trend and decay assumptions.

Finally, these estimators work very well with the transformers discussed in previous tutorials. Let’s demonstrate the compositional nature of these estimators.

wkcomp = (

cl.load_sample("clrd")

.groupby("LOB")

.sum()

.loc["wkcomp"][["CumPaidLoss", "EarnedPremNet"]]

)

wkcomp

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (1, 2, 10, 10) |

| Index: | [LOB] |

| Columns: | [CumPaidLoss, EarnedPremNet] |

Let’s calculate the age-to-age factors:

Without the the 1995 valuation period

Using volume weighted for the first 5 factors, and simple average for the next 4 factors (for a total of 9 age-to-age factors)

Using no more than 7 periods (with

n_periods)

patterns = cl.Pipeline(

[

(

"dev",

cl.Development(

average=["volume"] * 5 + ["simple"] * 4,

n_periods=7,

drop_valuation="1995",

),

),

("tail", cl.TailCurve(curve="inverse_power", extrap_periods=80)),

]

)

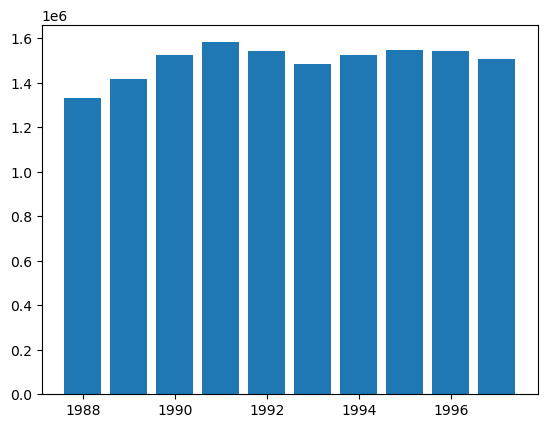

cc = cl.CapeCod(decay=0.8, trend=0.02).fit(

X=patterns.fit_transform(wkcomp["CumPaidLoss"]),

sample_weight=wkcomp["EarnedPremNet"].latest_diagonal,

)

cc.ultimate_

| 2261 | |

|---|---|

| 1988 | 1,331,221 |

| 1989 | 1,416,505 |

| 1990 | 1,523,470 |

| 1991 | 1,581,962 |

| 1992 | 1,541,458 |

| 1993 | 1,484,168 |

| 1994 | 1,525,963 |

| 1995 | 1,548,534 |

| 1996 | 1,541,068 |

| 1997 | 1,507,592 |

plt.bar(

cc.ultimate_.to_frame(origin_as_datetime=True).index.year,

cc.ultimate_.to_frame(origin_as_datetime=True)["2261"],

)

<BarContainer object of 10 artists>

Voting Chainladder#

A VotingChainladder is an ensemble meta-estimator that fits several base chainladder methods, each on the whole triangle. Then it combines the individual predictions based on a matrix of weights to form a final prediction.

Let’s begin by loading the raa dataset.

raa = cl.load_sample("raa")

Instantiate the Chainladder’s estimator.

cl_mod = cl.Chainladder()

Instantiate the Expected Loss’s estimator.

el_mod = cl.ExpectedLoss(apriori=1)

Instantiate the Bornhuetter-Ferguson’s estimator. Remember that the BornhuetterFerguson requires one argument, the apriori.

bf_mod = cl.BornhuetterFerguson(apriori=1)

Instantiate the Cape Cod’s estimator and their required arguments.

cc_mod = cl.CapeCod(decay=1, trend=0)

Instantiate the Benktander’s estimator and their required arguments.

bk_mod = cl.Benktander(apriori=1, n_iters=2)

Let’s prepare the estimators variable. The estimators parameter in VotingChainladder must be in an array of tuples, with (estimator_name, estimator) pairing.

estimators = [

("cl", cl_mod),

("el", el_mod),

("bf", bf_mod),

("cc", cc_mod),

("bk", bk_mod),

]

Recall that some estimators (in this case, BornhuetterFerguson, CapeCod, and Benktander) also require the variable sample_weight, let’s use the mean of Chainladder’s average ultimate estimate.

sample_weight = cl_mod.fit(raa).ultimate_ * 0 + (

float(cl_mod.fit(raa).ultimate_.sum()) / 10

)

sample_weight

| 2261 | |

|---|---|

| 1981 | 21,312 |

| 1982 | 21,312 |

| 1983 | 21,312 |

| 1984 | 21,312 |

| 1985 | 21,312 |

| 1986 | 21,312 |

| 1987 | 21,312 |

| 1988 | 21,312 |

| 1989 | 21,312 |

| 1990 | 21,312 |

model_weights = np.array(

[[0.6, 0, 0.2, 0.2, 0]] * 4 + [[0, 0, 0.5, 0.5, 0]] * 3 + [[0, 0, 0, 1, 0]] * 3

)

vot_mod = cl.VotingChainladder(estimators=estimators, weights=model_weights).fit(

raa, sample_weight=sample_weight

)

vot_mod.ultimate_

| 2261 | |

|---|---|

| 1981 | 18,834 |

| 1982 | 16,876 |

| 1983 | 24,059 |

| 1984 | 28,543 |

| 1985 | 28,237 |

| 1986 | 19,905 |

| 1987 | 18,947 |

| 1988 | 23,107 |

| 1989 | 20,005 |

| 1990 | 21,606 |

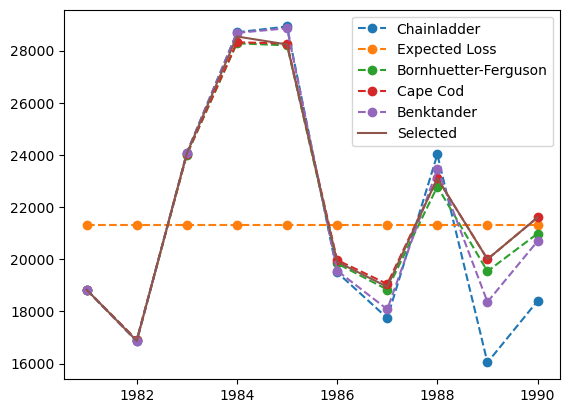

plt.plot(

cl_mod.fit(raa).ultimate_.to_frame(origin_as_datetime=True).index.year,

cl_mod.fit(raa).ultimate_.to_frame(origin_as_datetime=True),

label="Chainladder",

linestyle="dashed",

marker="o",

)

plt.plot(

el_mod.fit(raa, sample_weight=sample_weight)

.ultimate_.to_frame(origin_as_datetime=True)

.index.year,

el_mod.fit(raa, sample_weight=sample_weight).ultimate_.to_frame(

origin_as_datetime=True

),

label="Expected Loss",

linestyle="dashed",

marker="o",

)

plt.plot(

bf_mod.fit(raa, sample_weight=sample_weight)

.ultimate_.to_frame(origin_as_datetime=True)

.index.year,

bf_mod.fit(raa, sample_weight=sample_weight).ultimate_.to_frame(

origin_as_datetime=True

),

label="Bornhuetter-Ferguson",

linestyle="dashed",

marker="o",

)

plt.plot(

cc_mod.fit(raa, sample_weight=sample_weight)

.ultimate_.to_frame(origin_as_datetime=True)

.index.year,

cc_mod.fit(raa, sample_weight=sample_weight).ultimate_.to_frame(

origin_as_datetime=True

),

label="Cape Cod",

linestyle="dashed",

marker="o",

)

plt.plot(

bk_mod.fit(raa, sample_weight=sample_weight)

.ultimate_.to_frame(origin_as_datetime=True)

.index.year,

bk_mod.fit(raa, sample_weight=sample_weight).ultimate_.to_frame(

origin_as_datetime=True

),

label="Benktander",

linestyle="dashed",

marker="o",

)

plt.plot(

vot_mod.ultimate_.to_frame(origin_as_datetime=True).index.year,

vot_mod.ultimate_.to_frame(origin_as_datetime=True),

label="Selected",

)

plt.legend(loc="best")

<matplotlib.legend.Legend at 0x7f9fdb4dcd10>

We can also call the weights attribute to confirm the weights being used by the VotingChainladder ensemble model.

vot_mod.weights

array([[0.6, 0. , 0.2, 0.2, 0. ],

[0.6, 0. , 0.2, 0.2, 0. ],

[0.6, 0. , 0.2, 0.2, 0. ],

[0.6, 0. , 0.2, 0.2, 0. ],

[0. , 0. , 0.5, 0.5, 0. ],

[0. , 0. , 0.5, 0.5, 0. ],

[0. , 0. , 0.5, 0.5, 0. ],

[0. , 0. , 0. , 1. , 0. ],

[0. , 0. , 0. , 1. , 0. ],

[0. , 0. , 0. , 1. , 0. ]])