Extrapolation Period Sensitivity#

import chainladder as cl

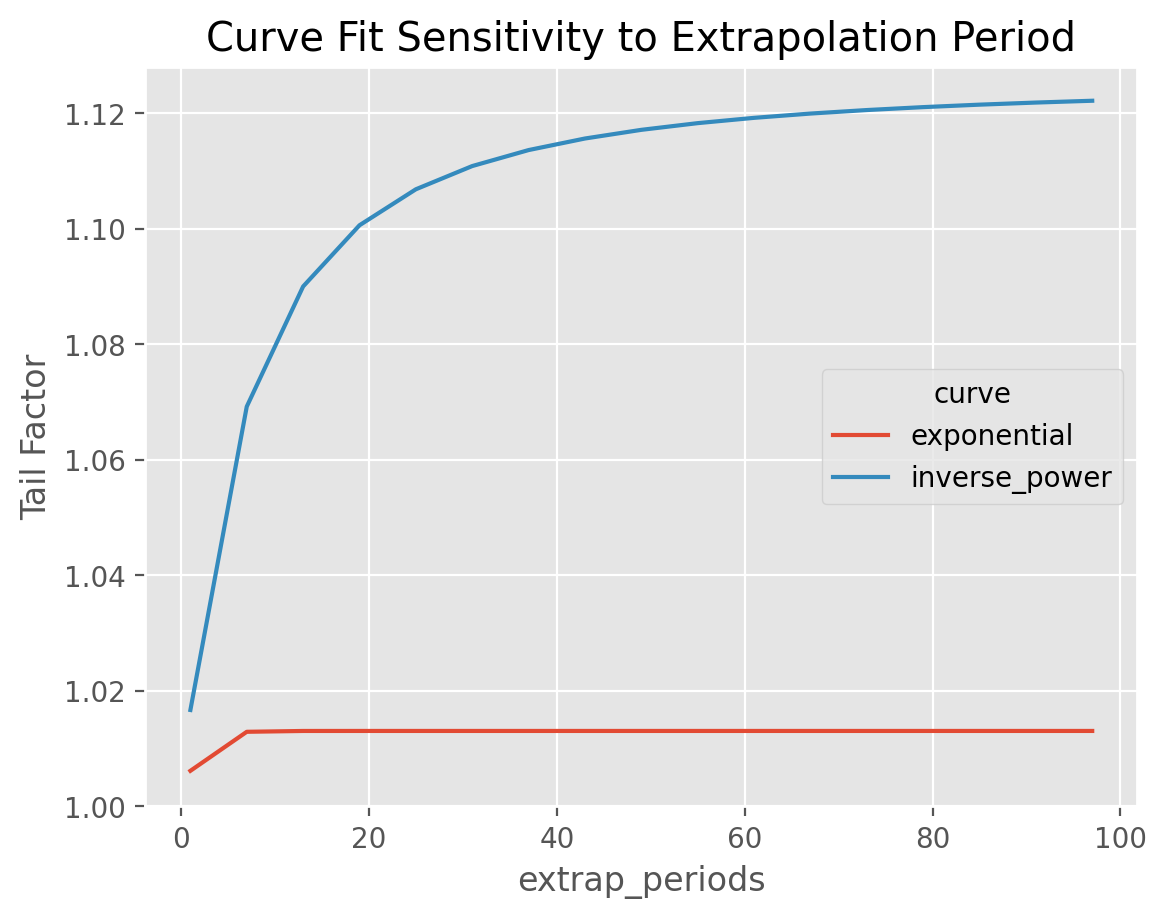

This example demonstrates the extrap_periods functionality of the TailCurve

estimator. The estimator defaults to extrapolating out 100 periods. However,

we can see that the “Inverse Power” curve fit doesn’t converge to its asymptotic

value.

tri = cl.load_sample('clrd').groupby('LOB').sum().loc['medmal', 'CumPaidLoss']

# Create a fuction to grab the scalar tail value.

def scoring(model):

""" Scoring functions must return a scalar """

return model.tail_.iloc[0, 0]

# Create a grid of scenarios

param_grid = dict(

extrap_periods=list(range(1, 100, 6)),

curve=['inverse_power', 'exponential'])

# Fit Grid

model = cl.GridSearch(cl.TailCurve(), param_grid=param_grid, scoring=scoring).fit(tri)

# Plot results

results = model.results_.pivot(columns='curve', index='extrap_periods', values='score')

Show code cell source

import matplotlib.pyplot as plt

plt.style.use('ggplot')

%config InlineBackend.figure_format = 'retina'

ax = results.plot(

ylim=(1,None), ylabel='Tail Factor',

title='Curve Fit Sensitivity to Extrapolation Period');