Triangle#

Introduction#

With this User Guide, we will be covering all of the core functionality of chainladder.

All important user functionality can be referenced from the top level of the library and

so importing the library as the cl namespace is the preferred way of importing from chainladder.

import chainladder as cl

import matplotlib.pyplot as plt

plt.style.use('ggplot')

%config InlineBackend.figure_format = 'retina'

Analysis is the intersection of data, models, and assumptions.

Reserving analysis is no different and the loss Triangle is the most ubiquitous data construct used by actuaries today. The chainladder package has its own :class:Triangle data structure that behaves much like a pandas DataFrame.

Why not Pandas?#

This begs the question, why not just use pandas? There are several advantages over having a dedicated Triangle object:

Actuaries work with sets of triangles. DataFrames, being two dimensional, support single triangles with grace but become unwieldy with multiple triangles.

We can carry through the meaningful pandas functionality while also supporting triangle specific methods not found in pandas

Improved memory footprint with sparse array representation in backend

Calculated fields with “virtual” columns allows for lazy column evaluation of Triangles as well as improved memory footprint for larger triangles.

Ability to support GPU-based backends.

Ultimately, there are a lot of things pandas can do that are not relevant to reserving, and there are a lot of things a Triangle needs to do that are not handled easily with pandas.

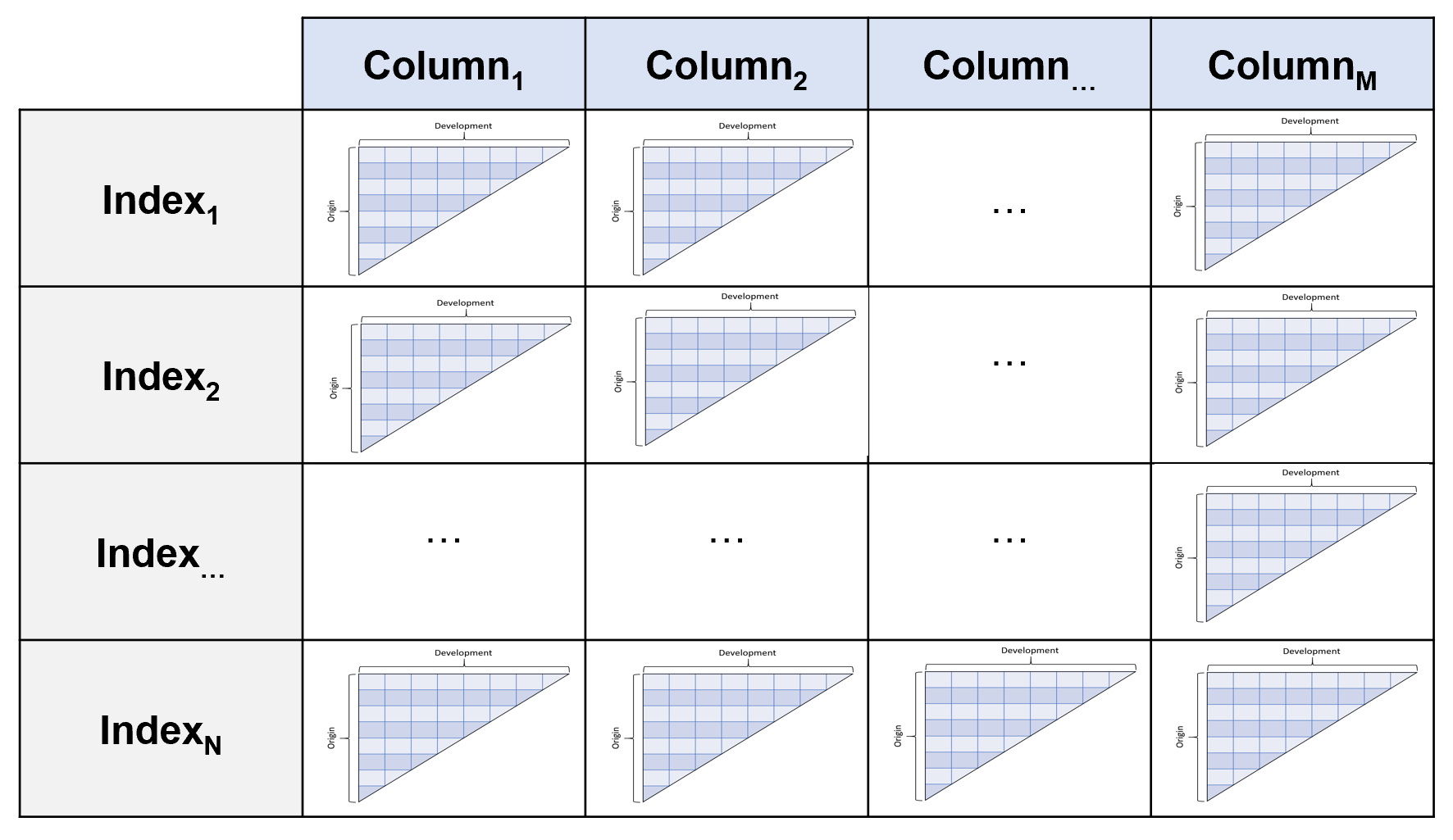

Structure#

The :class:Triangle is the data structure of the chainladder package. Just as

Scikit-learn likes to only consume numpy arrays, Chainladder only likes

Triangles. It is a 4D data structure with labeled axes. These axes are its

index, columns, origin, development.

index (axis 0):

The index is the lowest grain at which you want to manage the triangle.

These can be things like state or company. Like a pandas.multiIndex, you

can throw more than one column into the index.

columns (axis 1):

Columns are where you would want to store the different numeric values of your

data. Paid, Incurred, Counts are all reasonable choices for the columns of your

triangle.

origin (axis 2):

The origin is the period of time from which your columns originate. It can

be an Accident Month, Report Year, Policy Quarter or any other period-like vector.

development (axis 3):

Development represents the development age or date of your triangle.

Valuation Month, Valuation Year, Valuation Quarter are good choices.

Despite this structure, you interact with it in the style of pandas. You would

use index and columns in the same way you would for a pandas DataFrame.

You can think of the 4D structure as a pandas DataFrame where each cell (row,

column) is its own triangle.

Like pandas, you can access the values property of a triangle to get its numpy

representation, however the Triangle class provides many helper methods to

keep the shape of the numpy representation in sync with the other Triangle

properties.

Creating a Triangle#

Basic requirements#

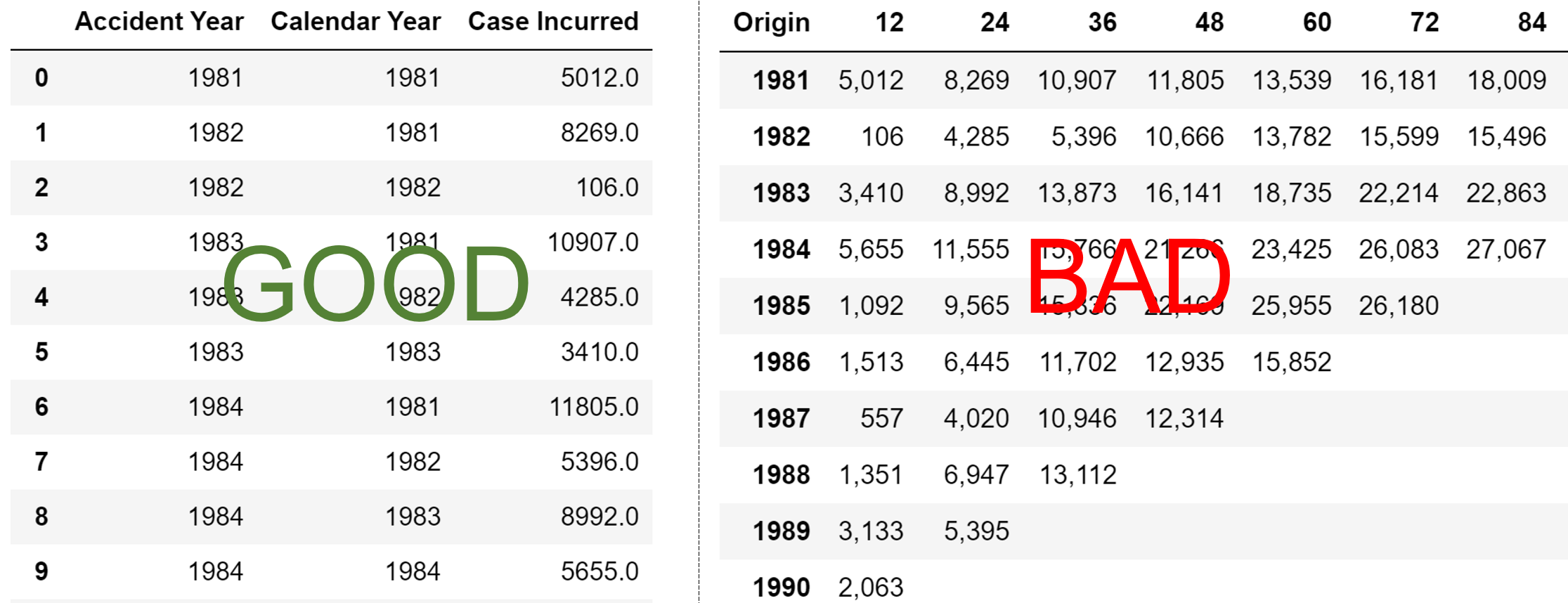

You must have a pandas DataFrame on hand to create a triangle. While data can come in a variety of forms those formats should be coerced to a pandas DataFrame before creating a triangle. The DataFrame also must be in tabular (long) format, not triangle (wide) format:

At a minimum, the DataFrame must also:

have “date-like” columns for the

originanddevelopmentperiod of the triangle.Have a numeric column(s) representing the amount(s) of the triangle.

The reason for these restriction is that the :class:Triangle infers a lot of

useful properties from your DataFrame. For example, it will determine the grain

and valuation_date of your triangle which in turn are used to derive many

other properties of your triangle without further prompting from you.

Date Inference#

When instantiating a :class:Triangle, the origin and development

arguments can take a str representing the column name in your pandas DataFrame

that contains the relevant information. Alternatively, the arguments can also

take a list in the case where your DataFrame includes multiple columns that

represent the dimension, e.g. ['accident_year','accident_quarter'] can be

supplied to create an origin dimension at the accident quarter grain.

cl.Triangle(data, origin='Acc Year', development=['Cal Year', 'Cal Month'], columns=['Paid Loss'])

The :class:Triangle relies heavily on pandas date inference. In fact,

pd.to_datetime(date_like) is exactly how it works. While pandas is excellent

at inference, it is not perfect. When initializing a Triangle you can always

use the origin_format and/or development_format arguments to force

the inference. For example, origin_format='%Y/%m/%d'

Multidimensional Triangle#

So far we’ve seen how to create a single Triangle, but as described in the Intro

the Triangle class can hold multiple triangles at once. These triangles share the

same origin and development axes and act as individual cells would in a

pandas DataFrame. By specifying one or more column and one or more index,

we can fill out the 4D triangle structure.

cl.Triangle(data, origin='Acc Year', development='Cal Year',

columns=['Paid Loss', 'Incurred Loss'],

index=['Line of Business', 'State'])

Sample Data#

The chainladder package has several sample triangles. Many of these come

from existing papers and can be used to verify the results of those papers.

Additionally, They are a quick way of exploring the functionality of the package.

These triangles can be called by name using the :func:~chainladder.load_sample function.

cl.load_sample('clrd')

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (775, 6, 10, 10) |

| Index: | [GRNAME, LOB] |

| Columns: | [IncurLoss, CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet] |

Other Parameters#

Whether a triangle is cumulative or incremental in nature cannot be inferred

from the “date-like” vectors of your DataFrame. You can optionally specify this

property with the cumulative parameter.

cl.Triangle(

data, origin='Acc Year', development=['Cal Year'],

columns=['PaidLoss'], cumulative=True)

Note

The cumulative parameter is completely optional. If it is not specified,

the Triangle will infer its cumulative/incremental status at the point you

call on the cum_to_incr or incr_to_cum methods discussed below. Some methods

may not work until the cumulative/incremental status is known.

Backends

Triangle is built on numpy which serves as the array backend by default.

However, you can now swap array_backend between numpy, cupy, and sparse to switch

between CPU and GPU-based computations or dense and sparse backends.

Array backends can be set globally:

cl.options.set_option('array_backend', 'cupy')

cl.options.reset_option()

Alternatively, they can be set per Triangle instance.

cl.Triangle(..., array_backend='cupy')

Note

You must have a CUDA-enabled graphics card and CuPY installed to use the GPU backend. These are optional dependencies of chainladder.

Chainladder by default will swap between the numpy and sparse backends. This

substantially improves the memory footprint of chainladder substantially beyond

what can be achieved with pandas alone. When a Triangle becomes sufficiently large

and has a lot of 0 or null entries, the triangle will silently swap between the

numpy and sparse backends.

prism = cl.load_sample('prism')

prism

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

| Triangle Summary | |

|---|---|

| Valuation: | 2017-12 |

| Grain: | OMDM |

| Shape: | (34244, 4, 120, 120) |

| Index: | [ClaimNo, Line, Type, ClaimLiability, Limit, Deductible] |

| Columns: | [reportedCount, closedPaidCount, Paid, Incurred] |

prism.array_backend

'sparse'

prism.sum().array_backend

'numpy'

You can globally disable the backend swapping by invoking auto_sparse(False).

Any triangle with a cupy backend will not invoke auto_sparse. In the future it may be supported

when there is better sparse-GPU array support.:

cl.options.set_option('auto_sparse', False)

prism = cl.load_sample('prism', array_backend='sparse')

prism.array_backend

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

'sparse'

prism.sum().array_backend

'numpy'

Warning

Loading ‘prism’ with the numpy backend will consume all of your systems memory.

Basic Functionality#

Representation#

The Triangle has two different representations. When only a single

index AND single column is selected. The triangle is the typical 2-dimensional

representation we typically think of.

triangle = cl.load_sample('ukmotor')

print(triangle.shape)

triangle

(1, 1, 7, 7)

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | |

|---|---|---|---|---|---|---|---|

| 2007 | 3,511 | 6,726 | 8,992 | 10,704 | 11,763 | 12,350 | 12,690 |

| 2008 | 4,001 | 7,703 | 9,981 | 11,161 | 12,117 | 12,746 | |

| 2009 | 4,355 | 8,287 | 10,233 | 11,755 | 12,993 | ||

| 2010 | 4,295 | 7,750 | 9,773 | 11,093 | |||

| 2011 | 4,150 | 7,897 | 10,217 | ||||

| 2012 | 5,102 | 9,650 | |||||

| 2013 | 6,283 |

If more than one index or more than one column is present, then the Triangle

takes on more of a summary view.

triangle = cl.load_sample('CLRD')

print(triangle.shape)

triangle

(775, 6, 10, 10)

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (775, 6, 10, 10) |

| Index: | [GRNAME, LOB] |

| Columns: | [IncurLoss, CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet] |

Valuation vs Development#

While most Estimators that use triangles expect the development period to be

expressed as an origin age, it is possible to transform a triangle into a valuation

triangle where the development periods are converted to valuation periods. Expressing

triangles this way may provide a more convenient view of valuation slices.

Switching between a development triangle and a valuation triangle can be

accomplished with the method dev_to_val and its inverse val_to_dev.

cl.load_sample('raa').dev_to_val()

| 1981 | 1982 | 1983 | 1984 | 1985 | 1986 | 1987 | 1988 | 1989 | 1990 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1981 | 5,012 | 8,269 | 10,907 | 11,805 | 13,539 | 16,181 | 18,009 | 18,608 | 18,662 | 18,834 |

| 1982 | 106 | 4,285 | 5,396 | 10,666 | 13,782 | 15,599 | 15,496 | 16,169 | 16,704 | |

| 1983 | 3,410 | 8,992 | 13,873 | 16,141 | 18,735 | 22,214 | 22,863 | 23,466 | ||

| 1984 | 5,655 | 11,555 | 15,766 | 21,266 | 23,425 | 26,083 | 27,067 | |||

| 1985 | 1,092 | 9,565 | 15,836 | 22,169 | 25,955 | 26,180 | ||||

| 1986 | 1,513 | 6,445 | 11,702 | 12,935 | 15,852 | |||||

| 1987 | 557 | 4,020 | 10,946 | 12,314 | ||||||

| 1988 | 1,351 | 6,947 | 13,112 | |||||||

| 1989 | 3,133 | 5,395 | ||||||||

| 1990 | 2,063 |

Triangles have the is_val_tri property that denotes whether a triangle is in valuation

mode. The latest diagonal of a Triangle is a valuation triangle.

cl.load_sample('raa').latest_diagonal.is_val_tri

True

Incremental vs Cumulative#

A triangle is either cumulative or incremental. The is_cumulative

property will identify this trait. Accumulating an incremental triangle can

be acomplished with incr_to_cum. The inverse operation is cum_to_incr.

raa = cl.load_sample('raa')

print(raa.is_cumulative)

raa.cum_to_incr()

True

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1981 | 5,012 | 3,257 | 2,638 | 898 | 1,734 | 2,642 | 1,828 | 599 | 54 | 172 |

| 1982 | 106 | 4,179 | 1,111 | 5,270 | 3,116 | 1,817 | -103 | 673 | 535 | |

| 1983 | 3,410 | 5,582 | 4,881 | 2,268 | 2,594 | 3,479 | 649 | 603 | ||

| 1984 | 5,655 | 5,900 | 4,211 | 5,500 | 2,159 | 2,658 | 984 | |||

| 1985 | 1,092 | 8,473 | 6,271 | 6,333 | 3,786 | 225 | ||||

| 1986 | 1,513 | 4,932 | 5,257 | 1,233 | 2,917 | |||||

| 1987 | 557 | 3,463 | 6,926 | 1,368 | ||||||

| 1988 | 1,351 | 5,596 | 6,165 | |||||||

| 1989 | 3,133 | 2,262 | ||||||||

| 1990 | 2,063 |

Triangle Grain#

If your triangle has origin and development grains that are more frequent then

yearly, you can easily swap to a higher grain using the grain method of the

Triangle. The grain method recognizes Yearly (Y), Quarterly (Q), and

Monthly (M) grains for both the origin period and development period.

cl.load_sample('quarterly')

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: Could not infer format, so each element will be parsed individually, falling back to `dateutil`. To ensure parsing is consistent and as-expected, please specify a format.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

| Triangle Summary | |

|---|---|

| Valuation: | 2006-03 |

| Grain: | OYDQ |

| Shape: | (1, 2, 12, 45) |

| Index: | [Total] |

| Columns: | [incurred, paid] |

cl.load_sample('quarterly').grain('OYDY')

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: Could not infer format, so each element will be parsed individually, falling back to `dateutil`. To ensure parsing is consistent and as-expected, please specify a format.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

| Triangle Summary | |

|---|---|

| Valuation: | 2006-03 |

| Grain: | OYDY |

| Shape: | (1, 2, 12, 12) |

| Index: | [Total] |

| Columns: | [incurred, paid] |

It is generally a good practice to bring your data in at the lowest grain available, so that you have full flexibility in aggregating to the grain of your choosing for analysis and separately, the grain of your choosing for reporting and communication.

Link Ratios#

The age-to-age factors or link ratios of a Triangle can be accessed with the

link_ratio property. Triangles also have a heatmap method that can optionally

be called to apply conditional formatting to triangle values along an axis. The

heatmap method requires IPython/Jupyter notebook to render.

triangle = cl.load_sample('abc')

triangle.link_ratio.heatmap()

| 12-24 | 24-36 | 36-48 | 48-60 | 60-72 | 72-84 | 84-96 | 96-108 | 108-120 | 120-132 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1977 | 2.2263 | 1.3933 | 1.1835 | 1.1070 | 1.0679 | 1.0468 | 1.0304 | 1.0231 | 1.0196 | 1.0163 |

| 1978 | 2.2682 | 1.3924 | 1.1857 | 1.1069 | 1.0649 | 1.0451 | 1.0301 | 1.0267 | 1.0207 | |

| 1979 | 2.2331 | 1.4014 | 1.1871 | 1.1068 | 1.0649 | 1.0418 | 1.0352 | 1.0276 | ||

| 1980 | 2.1988 | 1.3944 | 1.2021 | 1.1014 | 1.0702 | 1.0496 | 1.0394 | |||

| 1981 | 2.2115 | 1.4004 | 1.1764 | 1.1094 | 1.0706 | 1.0536 | ||||

| 1982 | 2.2290 | 1.3872 | 1.2037 | 1.1264 | 1.0956 | |||||

| 1983 | 2.2918 | 1.4296 | 1.2197 | 1.1337 | ||||||

| 1984 | 2.3731 | 1.4654 | 1.2283 | |||||||

| 1985 | 2.4457 | 1.4704 | ||||||||

| 1986 | 2.4031 |

The Triangle link_ratio property has unique properties from regular triangles.

They are considered patterns.

triangle.link_ratio.is_pattern

True

They are considered incremental, and accumulate in a multiplicative fashion.

triangle = cl.load_sample('abc')

triangle.link_ratio.incr_to_cum()

| 12-Ult | 24-Ult | 36-Ult | 48-Ult | 60-Ult | 72-Ult | 84-Ult | 96-Ult | 108-Ult | 120-Ult | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1977 | 4.9633 | 2.2293 | 1.6000 | 1.3519 | 1.2213 | 1.1436 | 1.0924 | 1.0601 | 1.0362 | 1.0163 |

| 1978 | 4.9795 | 2.1954 | 1.5767 | 1.3298 | 1.2014 | 1.1282 | 1.0795 | 1.0479 | 1.0207 | |

| 1979 | 4.8528 | 2.1731 | 1.5507 | 1.3063 | 1.1802 | 1.1083 | 1.0638 | 1.0276 | ||

| 1980 | 4.7394 | 2.1555 | 1.5458 | 1.2859 | 1.1675 | 1.0910 | 1.0394 | |||

| 1981 | 4.5594 | 2.0616 | 1.4722 | 1.2514 | 1.1280 | 1.0536 | ||||

| 1982 | 4.5932 | 2.0607 | 1.4855 | 1.2341 | 1.0956 | |||||

| 1983 | 4.5302 | 1.9767 | 1.3827 | 1.1337 | ||||||

| 1984 | 4.2715 | 1.8000 | 1.2283 | |||||||

| 1985 | 3.5962 | 1.4704 | ||||||||

| 1986 | 2.4031 |

Commutativity#

Where possible, the triangle methods are designed to be commutative. For example, each of these operations is functionally equivalent.

tri = cl.load_sample('quarterly')

# Functionally equivalent transformations

tri.grain('OYDY').val_to_dev() == tri.val_to_dev().grain('OYDY')

tri.cum_to_incr().grain('OYDY').val_to_dev() == tri.val_to_dev().cum_to_incr().grain('OYDY')

tri.grain('OYDY').cum_to_incr().val_to_dev().incr_to_cum() == tri.val_to_dev().grain('OYDY')

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: Could not infer format, so each element will be parsed individually, falling back to `dateutil`. To ensure parsing is consistent and as-expected, please specify a format.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

True

Performance Tips#

Being mindful of commutativity and computational intensity can really help improve the performance of the package, particularly for really large triangles. Consider these examples that produce identical outputs but with drastically different performance. In general, aggregations reduce the number of cells in a Triangle and should come as early in your method chain as possible.

import timeit

prism = cl.load_sample('prism')

# Accumulation before aggregation - BAD

timeit.timeit(lambda : prism.incr_to_cum().sum(), number=1)

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/base.py:250: UserWarning: The argument 'infer_datetime_format' is deprecated and will be removed in a future version. A strict version of it is now the default, see https://pandas.pydata.org/pdeps/0004-consistent-to-datetime-parsing.html. You can safely remove this argument.

arr = dict(zip(datetime_arg, pd.to_datetime(**item)))

10.157972535999988

# Aggregation before accumulation - GOOD

timeit.timeit(lambda : prism.sum().incr_to_cum(), number=1)

0.02395860700016783

In other cases, querying the Triangle in clever ways can improve performance.

Consider that the latest_diagonal of a cumulative Triangle is equal to the

sum of its incremental values along the ‘development’ axis.

# Accumulating a large triangle to get latest_diagonal - BAD

timeit.timeit(lambda : prism.incr_to_cum().latest_diagonal, number=1)

9.175006923999945

# Summing incrementals of a large triangle to get latest_diagonal - GOOD

timeit.timeit(lambda : prism.sum('development'), number=1)

0.03220626000006632

Trend#

A uniform trend factor can also be applied to a Triangle. The trend can

be applied along the origin or valuation axes.

tri = cl.load_sample('ukmotor')

# Dividing by original triangle to show the trend factor

tri.trend(0.05, axis='valuation')/tri

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | |

|---|---|---|---|---|---|---|---|

| 2007 | 1.3401 | 1.2763 | 1.2155 | 1.1576 | 1.1025 | 1.0500 | 1.0000 |

| 2008 | 1.2763 | 1.2155 | 1.1576 | 1.1025 | 1.0500 | 1.0000 | |

| 2009 | 1.2155 | 1.1576 | 1.1025 | 1.0500 | 1.0000 | ||

| 2010 | 1.1576 | 1.1025 | 1.0500 | 1.0000 | |||

| 2011 | 1.1025 | 1.0500 | 1.0000 | ||||

| 2012 | 1.0500 | 1.0000 | |||||

| 2013 | 1.0000 |

While the trend method only allows for a single trend, you can create

compound trends using start and end arguments and chaining them together.

tri.trend(0.05, axis='valuation', start=tri.valuation_date, end='2011-12-31') \

.trend(0.10, axis='valuation', start='2011-12-31')/tri

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | |

|---|---|---|---|---|---|---|---|

| 2007 | 1.6142 | 1.4674 | 1.3340 | 1.2128 | 1.1025 | 1.0500 | 1.0000 |

| 2008 | 1.4674 | 1.3340 | 1.2128 | 1.1025 | 1.0500 | 1.0000 | |

| 2009 | 1.3340 | 1.2127 | 1.1025 | 1.0500 | 1.0000 | ||

| 2010 | 1.2128 | 1.1025 | 1.0500 | 1.0000 | |||

| 2011 | 1.1025 | 1.0500 | 1.0000 | ||||

| 2012 | 1.0500 | 1.0000 | |||||

| 2013 | 1.0000 |

Correlation Tests#

The multiplicative chainladder method is based on the strong assumptions of independence across origin years and across valuation years. Mack developed tests to verify if these assumptions hold.

These tests are included as methods on the triangle class valuation_correlation

and development_correlation. False indicates that correlation between years

is not sufficiently large.

triangle = cl.load_sample('raa')

triangle.valuation_correlation().z_critical

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/numpy/lib/nanfunctions.py:1217: RuntimeWarning: All-NaN slice encountered

return function_base._ureduce(a, func=_nanmedian, keepdims=keepdims,

| 1982 | 1983 | 1984 | 1985 | 1986 | 1987 | 1988 | 1989 | 1990 | |

|---|---|---|---|---|---|---|---|---|---|

| 1981 | False | False | False | False | False | False | False | False | False |

triangle.development_correlation().t_critical

There are many properties of these correlation tests and they’ve been included

as their own classes. Refer to ValuationCorrelation and

DevelopmentCorrelation for additional information.

Pandas-style syntax#

We’ve chosen to keep as close as possible to pandas syntax for Triangle data

manipulation. Relying on the most widely used data manipulation library in Python

gives us two benefits. This not only allows for easier adoption, but also provides

stability to the chainladder API.

Slicing and Filtering#

With a newly minted Triangle, individual triangles can be sliced out

of the object using pandas-style loc/iloc or boolean filtering.

clrd = cl.load_sample('clrd')

clrd.iloc[0,1]

clrd[clrd['LOB']=='othliab']

clrd['EarnedPremDIR']

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (775, 1, 10, 10) |

| Index: | [GRNAME, LOB] |

| Columns: | [EarnedPremDIR] |

Note

Boolean filtering on non-index columns in pandas feels natural. We’ve exposed

the same syntax specifically for the index column(s) of the Triangle without the

need for reset_index() or trying to boolean-filter a MultiIndex. This is

a divergence from the pandas API.

As of version 0.7.6, four-dimensional slicing is supported:

clrd = cl.load_sample('clrd')

clrd.iloc[[0, 10, 3], 1:8, :5, :]

clrd.loc[:'Aegis Grp', 'CumPaidLoss':, '1990':'1994', :48]

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (5, 5, 5, 4) |

| Index: | [GRNAME, LOB] |

| Columns: | [CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet] |

As of version 0.8.3, .iat and at functionality have been added. Similar

to pandas, one can use these for value assignment for a single cell of a Triangle.

When a ‘sparse’ backend is in use, these accessors are the only way to modify individual

cells of a triangle.

raa = cl.load_sample('raa').set_backend('sparse')

# To modify a sparse triangle, we need to use at or iat

raa.at['Total', 'values', '1985', 12] = 10000

Arithmetic#

Most arithmetic operations can be used to create new triangles within your

triangle instance. Like with pandas, these can automatically be added as new

columns to your Triangle.

clrd = cl.load_sample('clrd')

clrd['CaseIncur'] = clrd['IncurLoss']-clrd['BulkLoss']

clrd

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (775, 7, 10, 10) |

| Index: | [GRNAME, LOB] |

| Columns: | [IncurLoss, CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet, CaseIncur] |

For origin and development axes, arithmetic follows numpy broadcasting <https://numpy.org/doc/1.18/user/theory.broadcasting.html#array-broadcasting-in-numpy>_

rules. If broadcasting fails, arithmetic operations will rely on origin and

development vectors to determine whether an operation is legal.

raa = cl.load_sample('raa')

# Allow for arithmetic beyond numpy broadcasting rules

raa[raa.origin<'1985']+raa[raa.origin>='1985']

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1981 | 5,012 | 8,269 | 10,907 | 11,805 | 13,539 | 16,181 | 18,009 | 18,608 | 18,662 | 18,834 |

| 1982 | 106 | 4,285 | 5,396 | 10,666 | 13,782 | 15,599 | 15,496 | 16,169 | 16,704 | |

| 1983 | 3,410 | 8,992 | 13,873 | 16,141 | 18,735 | 22,214 | 22,863 | 23,466 | ||

| 1984 | 5,655 | 11,555 | 15,766 | 21,266 | 23,425 | 26,083 | 27,067 | |||

| 1985 | 1,092 | 9,565 | 15,836 | 22,169 | 25,955 | 26,180 | ||||

| 1986 | 1,513 | 6,445 | 11,702 | 12,935 | 15,852 | |||||

| 1987 | 557 | 4,020 | 10,946 | 12,314 | ||||||

| 1988 | 1,351 | 6,947 | 13,112 | |||||||

| 1989 | 3,133 | 5,395 | ||||||||

| 1990 | 2,063 |

# Numpy broadcasting equivalent fails

raa[raa.origin<'1985'].values+raa[raa.origin>='1985'].values

Arithmetic between two Triangles with different labels will align the axes of each Triangle consistent with arithmetic of a pandas Series. Bypassing index matching can be accomplished with arithmetic between an Triangle and an array.

s1 = cl.load_sample('clrd').iloc[:3]

s2 = s1.sort_index(ascending=False)

s1 + s2 == 2 * s1

True

s1 + s2.values == 2 * s1

False

s3 = s1.iloc[:, ::-1]

s1 + s3 == 2 * s1

True

Virtual Columns#

There are instances where we want to defer calculations, we can create “virtual” columns that defer calculation to when needed. These columns can be created by wrapping a normal column in a function. Lambda expressions work as a tidy representation of virtual columns.

clrd = cl.load_sample('clrd')

# A physical column with immediate evaluation

clrd['PaidLossRatio'] = clrd['CumPaidLoss'] / clrd['EarnedPremDIR']

# A virtual column with deferred evaluation

clrd['PaidLossRatio'] = lambda clrd : clrd['CumPaidLoss'] / clrd['EarnedPremDIR']

# Good - Defer loss ratio calculation until after summing premiums and losses

clrd.sum()['PaidLossRatio']

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1988 | 0.2424 | 0.4783 | 0.5980 | 0.6682 | 0.7097 | 0.7327 | 0.7449 | 0.7515 | 0.7569 | 0.7591 |

| 1989 | 0.2517 | 0.4901 | 0.6115 | 0.6829 | 0.7240 | 0.7457 | 0.7576 | 0.7651 | 0.7687 | |

| 1990 | 0.2548 | 0.4903 | 0.6114 | 0.6806 | 0.7168 | 0.7368 | 0.7488 | 0.7547 | ||

| 1991 | 0.2364 | 0.4558 | 0.5673 | 0.6311 | 0.6658 | 0.6839 | 0.6938 | |||

| 1992 | 0.2423 | 0.4601 | 0.5671 | 0.6266 | 0.6598 | 0.6765 | ||||

| 1993 | 0.2463 | 0.4618 | 0.5644 | 0.6227 | 0.6538 | |||||

| 1994 | 0.2523 | 0.4602 | 0.5592 | 0.6159 | ||||||

| 1995 | 0.2478 | 0.4445 | 0.5363 | |||||||

| 1996 | 0.2459 | 0.4280 | ||||||||

| 1997 | 0.2383 |

Virtual column expressions should only reference other columns in the same triangle. A Triangle without all the underlying columns will fail.

# Eliminating EarnedPremDIR will result in a calculation failure

clrd[['CumPaidLoss', 'PaidLossRatio']].sum()['PaidLossRatio']

When used in tandem with the ‘sparse’ backend, virtual columns can also substantially reduce the memory footprint of your Triangle. This is because the calculation expression is the only thing in memory.

Aggregations#

It is generally good practice to bring your data into chainladder at a ganularity

that is comfortably supported by your system RAM. This provides the greatest flexibility

in analyzing your data within the chainladder framework. However, not everything

needs to be analyzed at the most granular level. Like pandas, you can aggregate

multiple triangles within a Triangle by using sum() which can

optionally be coupled with groupby().

clrd = cl.load_sample('clrd')

clrd.sum()

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (1, 6, 10, 10) |

| Index: | [GRNAME, LOB] |

| Columns: | [IncurLoss, CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet] |

clrd.groupby('LOB').sum()

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (6, 6, 10, 10) |

| Index: | [LOB] |

| Columns: | [IncurLoss, CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet] |

By default, the aggregation will apply to the first axis with a length greater

than 1. Alternatively, you can specify the axis using the axis argument of

the aggregate method.

Like pandas, the groupby method supports any groupable list. This allows for

complex groupings that can be derived dynamically.

clrd = cl.load_sample('clrd')

clrd = clrd[clrd['LOB']=='comauto']

# Identify the largest commercial auto carriers (by premium) for 1997

top_10 = clrd['EarnedPremDIR'].groupby('GRNAME').sum().latest_diagonal.loc[..., '1997', :].to_frame().nlargest(10)

# Group any companies together that are not in the top 10

clrd.groupby(clrd.index['GRNAME'].map(lambda x: x if x in top_10.index else 'Remainder')).sum()

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (11, 6, 10, 10) |

| Index: | [GRNAME] |

| Columns: | [IncurLoss, CumPaidLoss, BulkLoss, EarnedPremDIR, EarnedPremCeded, EarnedPremNet] |

Converting to DataFrame#

When a triangle is presented with a single index level and single column, it

becomes a 2D object. As such, its display format changes to that similar to a

dataframe. These 2D triangles can easily be converted to a pandas dataframe

using the to_frame method.

clrd = cl.load_sample('clrd')

clrd[clrd['LOB']=='ppauto']['CumPaidLoss'].sum().to_frame()

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1988-01-01 | 3092818.0 | 5942711.0 | 7239089.0 | 7930109.0 | 8318795.0 | 8518201.0 | 8610355.0 | 8655509.0 | 8682451.0 | 8690036.0 |

| 1989-01-01 | 3556683.0 | 6753435.0 | 8219551.0 | 9018288.0 | 9441842.0 | 9647917.0 | 9753014.0 | 9800477.0 | 9823747.0 | NaN |

| 1990-01-01 | 4015052.0 | 7478257.0 | 9094949.0 | 9945288.0 | 10371175.0 | 10575467.0 | 10671988.0 | 10728411.0 | NaN | NaN |

| 1991-01-01 | 4065571.0 | 7564284.0 | 9161104.0 | 10006407.0 | 10419901.0 | 10612083.0 | 10713621.0 | NaN | NaN | NaN |

| 1992-01-01 | 4551591.0 | 8344021.0 | 10047179.0 | 10901995.0 | 11336777.0 | 11555121.0 | NaN | NaN | NaN | NaN |

| 1993-01-01 | 5020277.0 | 9125734.0 | 10890282.0 | 11782219.0 | 12249826.0 | NaN | NaN | NaN | NaN | NaN |

| 1994-01-01 | 5569355.0 | 9871002.0 | 11641397.0 | 12600432.0 | NaN | NaN | NaN | NaN | NaN | NaN |

| 1995-01-01 | 5803124.0 | 10008734.0 | 11807279.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1996-01-01 | 5835368.0 | 9900842.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1997-01-01 | 5754249.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

From this point the results can be operated on directly in pandas. The

to_frame functionality works when a Triangle is sliced down to any two axes

and is not limited to just the index and column.

clrd['CumPaidLoss'].groupby('LOB').sum().latest_diagonal.to_frame()

| origin | 1988 | 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | 1995 | 1996 | 1997 |

|---|---|---|---|---|---|---|---|---|---|---|

| LOB | ||||||||||

| comauto | 626097.0 | 674441.0 | 718396.0 | 711762.0 | 731033.0 | 762039.0 | 768095.0 | 675166.0 | 510191.0 | 272342.0 |

| medmal | 217239.0 | 222707.0 | 235717.0 | 275923.0 | 267007.0 | 276235.0 | 252449.0 | 209222.0 | 107474.0 | 20361.0 |

| othliab | 317889.0 | 350684.0 | 361103.0 | 426085.0 | 389250.0 | 434995.0 | 402244.0 | 294332.0 | 191258.0 | 54130.0 |

| ppauto | 8690036.0 | 9823747.0 | 10728411.0 | 10713621.0 | 11555121.0 | 12249826.0 | 12600432.0 | 11807279.0 | 9900842.0 | 5754249.0 |

| prodliab | 110973.0 | 112614.0 | 121255.0 | 100276.0 | 76059.0 | 94462.0 | 111264.0 | 62018.0 | 28107.0 | 10682.0 |

| wkcomp | 1241715.0 | 1308706.0 | 1394675.0 | 1414747.0 | 1328801.0 | 1187581.0 | 1114842.0 | 962081.0 | 736040.0 | 340132.0 |

The entire 4D triangle can be flattened to a DataFrame in long format. This can be handy for moving back and forth between pandas and chainladder.

Because chainladder only supports valuation dates when creating new triangles,

it is often helpful converting to a valuation format before moving to pandas.

clrd = cl.load_sample('clrd')

df = clrd.dev_to_val().cum_to_incr().to_frame()

df.head()

| origin | valuation | IncurLoss | CumPaidLoss | BulkLoss | EarnedPremDIR | EarnedPremCeded | EarnedPremNet | ||

|---|---|---|---|---|---|---|---|---|---|

| GRNAME | LOB | ||||||||

| Adriatic Ins Co | othliab | 1995-01-01 | 1995-12-31 23:59:59.999999999 | 8.0 | NaN | 8.0 | 139.0 | 131.0 | 8.0 |

| othliab | 1995-01-01 | 1996-12-31 23:59:59.999999999 | 3.0 | NaN | -4.0 | NaN | NaN | NaN | |

| othliab | 1995-01-01 | 1997-12-31 23:59:59.999999999 | -4.0 | 3.0 | NaN | NaN | NaN | NaN | |

| othliab | 1996-01-01 | 1996-12-31 23:59:59.999999999 | 40.0 | NaN | 40.0 | 410.0 | 359.0 | 51.0 | |

| othliab | 1997-01-01 | 1997-12-31 23:59:59.999999999 | 67.0 | NaN | 31.0 | 458.0 | 425.0 | 33.0 |

cl.Triangle(

df.reset_index(), index=['GRNAME', 'LOB'],

origin='origin', development='valuation',

columns=['BulkLoss', 'CumPaidLoss', 'EarnedPremCeded',

'EarnedPremDIR', 'EarnedPremNet', 'IncurLoss']

).incr_to_cum()

/home/docs/checkouts/readthedocs.org/user_builds/chainladder-python/conda/latest/lib/python3.11/site-packages/chainladder/core/triangle.py:189: UserWarning:

The cumulative property of your triangle is not set. This may result in

undesirable behavior. In a future release this will result in an error.

warnings.warn(

| Triangle Summary | |

|---|---|

| Valuation: | 1997-12 |

| Grain: | OYDY |

| Shape: | (775, 6, 10, 10) |

| Index: | [GRNAME, LOB] |

| Columns: | [BulkLoss, CumPaidLoss, EarnedPremCeded, EarnedPremDIR, EarnedPremNet, IncurLoss] |

To enforce long format when moving to pandas the keepdims argument guarantees

that all 4 dimensions of the Triangle will be preserved when moving to pandas.

cl.load_sample('raa').to_frame(keepdims=True).head()

| origin | development | values | |

|---|---|---|---|

| Total | |||

| Total | 1981-01-01 | 12 | 5012.0 |

| Total | 1981-01-01 | 24 | 8269.0 |

| Total | 1981-01-01 | 36 | 10907.0 |

| Total | 1981-01-01 | 48 | 11805.0 |

| Total | 1981-01-01 | 60 | 13539.0 |

Exposing Pandas functionality#

The ability to move from a triangle to a pandas DataFrame opens up the full

suite of pandas functionality to you. For the more commonly used

functionality, we handle the to_frame() for you. For example,

triangle.to_frame().plot() is equivalent to triangle.plot().

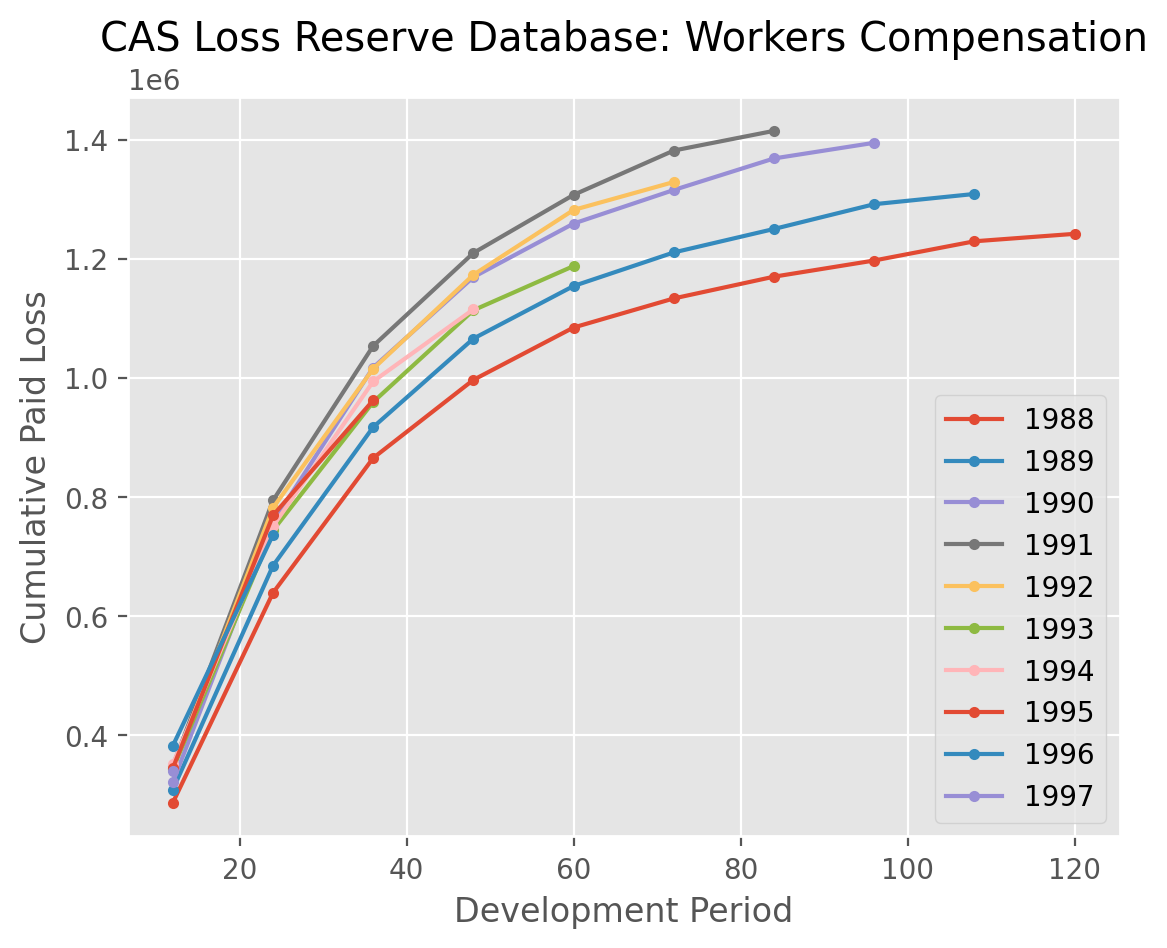

cl.load_sample('clrd').groupby('LOB').sum().loc['wkcomp', 'CumPaidLoss'].T.plot(

marker='.',

title='CAS Loss Reserve Database: Workers Compensation').set(

xlabel='Development Period', ylabel='Cumulative Paid Loss');

Many of the more commonly used pandas methods are passed through in this way allowing for working with triangles as DataFrames.

Aggregations |

IO |

Shaping |

Other |

|---|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|||

|

|||

|

Note

While some of these methods have been rewritten to return a Triangle, Many are pandas methods and will have return values consistent with pandas.

Accessors#

Like pandas .str and .dt accessor functions, you can also perform operations

on the origin, development or valuation of a triangle. For example, all

of these operations are legal.

raa = cl.load_sample('raa')

x = raa[raa.origin=='1986']

x = raa[(raa.development>=24)&(raa.development<=48)]

x = raa[raa.origin<='1985-JUN']

x = raa[raa.origin>'1987-01-01'][raa.development<=36]

x = raa[raa.valuation<raa.valuation_date]

These accessors apply boolean filtering along the origin or development of the

triangle. Because boolean filtering can only work on one axis at a time, you may

need to split up your indexing to achieve a desired result.

# Illegal use of boolean filtering of two different axes

x = raa[(raa.origin>'1987-01-01')&(raa.development<=36)]

# Instead, chain the boolean filters together.

x = raa[raa.origin>'1987-01-01'][raa.development<=36]

When using the accessors to filter a triangle, you may be left with empty portions

of the triangle that need to be trimmed up. The dropna method will look for

any origin periods or development periods that are fully empty at the edges

of the triangle and eliminate them for you.

raa = cl.load_sample('raa')

raa[raa.origin>'1987-01-01']

| 12 | 24 | 36 | 48 | 60 | 72 | 84 | 96 | 108 | 120 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1988 | 1,351 | 6,947 | 13,112 | |||||||

| 1989 | 3,133 | 5,395 | ||||||||

| 1990 | 2,063 |

There are many more methods available to manipulate triangles. The complete

list of methods is available under the Triangle docstrings.