TailCurve Basics#

import chainladder as cl

import pandas as pd

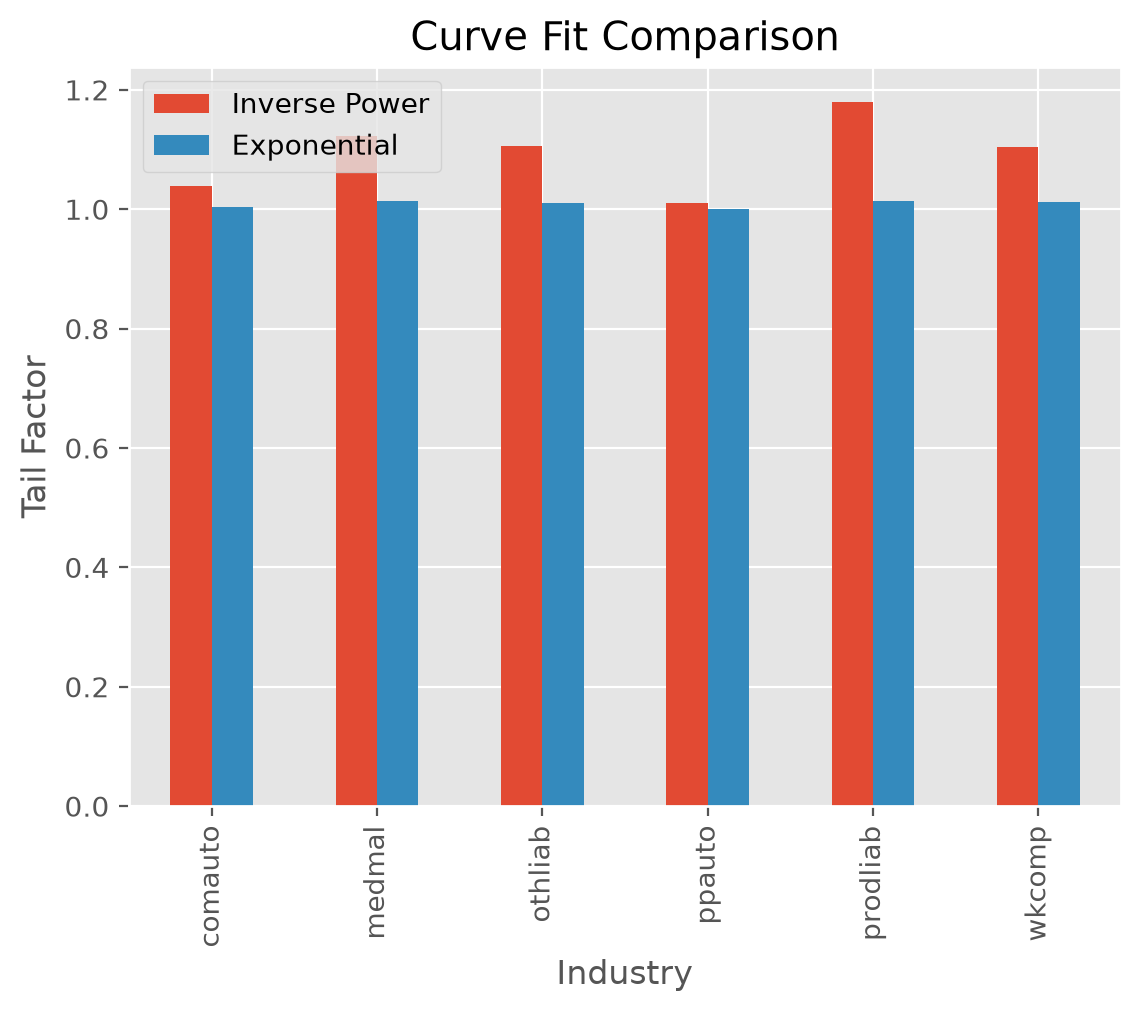

This example demonstrates how the inverse_power curve generally produces more

conservative tail factors than the exponential fit.

clrd = cl.load_sample('clrd').groupby('LOB').sum()['CumPaidLoss']

cdf_ip = cl.TailCurve(curve='inverse_power').fit(clrd)

cdf_xp = cl.TailCurve(curve='exponential').fit(clrd)

result = pd.concat((cdf_ip.tail_.rename("Inverse Power"),

cdf_xp.tail_.rename("Exponential")), axis=1)